Mag 7 issuances are a red flag

Welcome to MktContext! I am a professional money manager, trader, and investor who has been timing and beating the market for over a decade. We specialize in predicting market direction by studying the economy and market signals. Join 12,000 subscribers at MktContext.com for our weekly deep dives and analysis!

An important development happened this week in Mag7 land. Google is issuing shares, its first major equity raise since its IPO two decades ago. A share issuance involves creating new shares of its stock out of thin air, which the company sells to investors in order to raise funds. The funds can be used for anything, but in this case it’s almost certainly for building data centers.

Shortly after, Meta also unofficially considered an equity issuance to finance its aggressive AI buildout. Meta is known for overspending on big money-losing visionary projects like the Metaverse. So for them to raise funds is a big problem. Given the negative stock reaction to the announcement, we think Meta will reconsider this issuance.

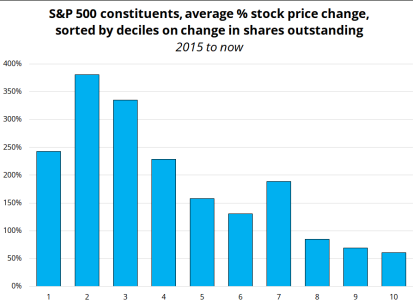

There is tons of academic research linking equity issuances to underperformance in stock returns. Companies with higher shares outstanding or bigger funding requirements also demonstrate weaker returns. This is empirical fact.

Moreover, they go from buyers of their own stock to sellers. It’s a simple supply/demand equation. More demand for shares = stock prices go up. More supply of shares = stock prices go down. We’ve discussed this problem in past posts:

“The other issue with diverting all cash flow to capex is it leaves little to buy back their own stock with. Given the copious amounts of idle cash they had before, stock buybacks were previously a major source of buying support. No buybacks means no price support. This explains the Mag 7’s awful stock performance in recent times.”

-From AI Capex Overheated, Feb 22, 2026

Seeing Mag7 issue shares is extra problematic. These companies have historically been cash-rich due to their lucrative asset-light business models (meaning it requires very little funding to grow). It highlights the shift from cash-generative to cash-burning entities all because of the enormous spending requirements of the AI boom. This makes them decidedly less valuable.

It doesn’t mean we immediately short the Mag7 companies. But one by one, the pillars of fundamental support for these stocks are eroding, until there is only air underneath them. They are sowing the seeds of their own implosion later down the road.

Read the rest of this article at MktContext.com

Join 12,000+ macro investors who get these insights before the mainstream media catches on!