The Great War Inflation Tax

What’s behind the numbers?

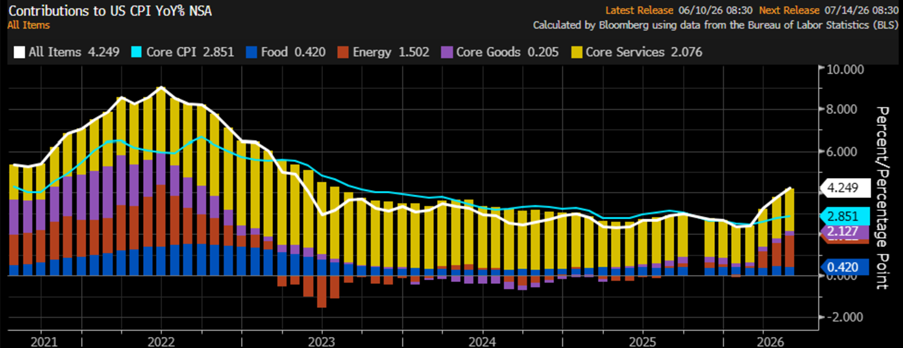

The fifth CPI print of the year delivered exactly what Wall Street ordered from the kitchen: a beautifully airbrushed +0.5% MoM, plated alongside a +4.2% YoY that landed right on consensus — and just happens to be the hottest reading since May 2023, back when the first inflation wave was supposedly “cooling” from the transitory fever that followed lockdowns and the war in Ukraine. But behind the soothing headline theatre, the understudy is stealing the show: energy accelerated again at +1.5%, its biggest annual jump since August 2022, when Western bureaucrats were busy sanctioning Russian oil with all the foresight of a man sawing off the branch he’s sitting on. Food and core goods, meanwhile, barely budged from April — the calm of a stage crew quietly resetting props between scenes.

Welcome to Act Two of Inflation Wave Two, where the orchestra tunes up while the audience insists the concert is over. Once fertilizer shortages and energy shocks finish leaking into the data, “temporary” may finally get the early retirement it’s been dodging for four years.

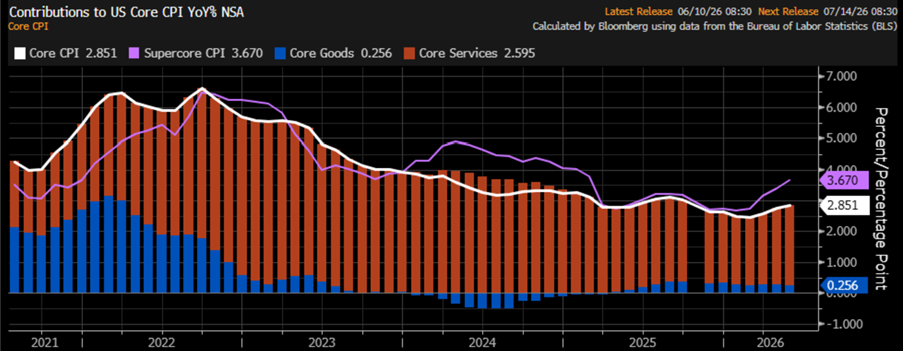

Core CPI delivered another thrilling episode of “nothing to worry about“: +0.2% MoM, a hair softer than expected, and +2.9% YoY — in line with forecast and a whisker above April’s +2.8% “transitory” print, because apparently inflation persistence is now considered a sign of economic resilience rather than a problem. The real star of the performance remained core services — the 76%-of-the-basket heavyweight that policymakers keep promising is “normalizing” — which instead quietly accelerated to +2.59%, its highest since last September, apparently unaware it had been scheduled for retirement. The official translation is that everything remains perfectly manageable, provided nobody commits the amateur mistake of looking at the trend. What the data is politely not shouting is that all types of shortages, energy spikes, and petrochemical supply-chain chaos have yet to arrive — and they do not do fashionably early. Enjoy this brief statistical intermission before the second inflation wave crashes through the consensus narrative like an uninvited guest who read the soft-landing forecast and laughed.

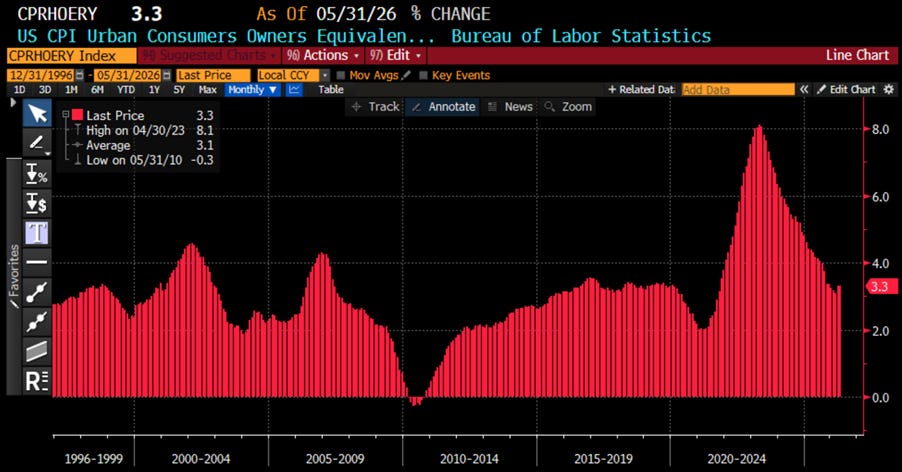

Cue the triumphant return of everyone’s favourite zombie metric: Owners’ Equivalent Rent — a number that measures the rent you would theoretically pay yourself for the house you actually own, and which the Bureau of Labor Statistics treats with the seriousness of peer-reviewed science — held steady at a proud +3.3% YoY in May, matching December’s pace and confirming that shelter inflation has now “stabilized” at a level that would have caused institutional cardiac arrest five years ago. Naturally, this is being packaged as a victory lap: the zombie is no longer sprinting, merely shuffling, and apparently that is the bar for success in 2026. Never mind that OER continues to quietly drain household purchasing power like a slow leak in a life raft — the important thing is that the number didn’t accelerate, which in modern central-bank dialect translates roughly as “nothing to see here until there is.” The “Inflation Is Dead” cheerleading squad is back on the field, pom-poms aloft, pointedly ignoring the corpse still warm on the floor.

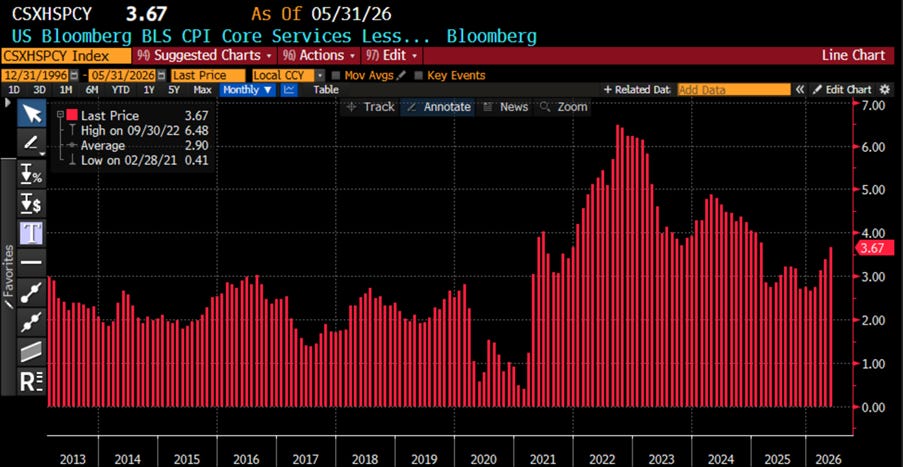

Adding another sparkling gem to the “Inflation Is Totally Dead, Trust Us” propaganda tour: SuperCore CPI — core services ex-housing, or as the Fed prefers to call it, “the only inflation metric that matters whenever the headline looks inconvenient” — just reaccelerated from April’s +3.38% YoY to a brisk +3.67%, a pace last spotted in December 2021, right before the 2022 stagflationary unpleasantness rudely interrupted the soft-landing fairy tale. This is the metric the Fed spent two years insisting was the truest signal of underlying price pressure — right up until it started accelerating again, at which point one suspects a new “most important metric” is already being workshopped in the basement of the Eccles Building. Translation: that wasn’t Mission Accomplished — it was a smoke break between inflation waves, and the cigarette is now firmly stubbed out. But by all means, keep reciting the victory sermon. Just politely ignore rent, food, goods, energy, insurance, and the radical extremism of basic arithmetic. Refill the daily hopium prescription, admire the emperor’s magnificent new clothes, and trust — as one always must — that this time the second wave will surely be different.

Thoughts.

May’s CPI will undoubtedly be marketed as another minor inconvenience courtesy of the Empire’s “tiny and totally successful” Middle East excursion — you know, the one declared won sometime around Hour 1 of Day 1, yet somehow still rattling global oil supply routes 100 days later and counting. Victory, it turns out, has become a subscription service. For ordinary Americans not employed by the Malthusian Washington Swamp plutocracy, however, grocery prices will continue their inspiring upward journey while energy costs remind everyone that “disinflation” was less an economic trend and more a seasonal marketing campaign. Inflation didn’t disappear — it just stopped to tie its shoes before sprinting into Wave Two, less than five years after the first one finished its victory lap. Meanwhile, policymakers and market cheerleaders keep toasting “transitory” while quietly assembling the next fiscal spending bonanza and geopolitical adventure package — because naturally, the cure for too much money chasing too few goods is even more money chasing even fewer goods. And here is the part that doesn’t make the press release: inflation and collapsing institutional trust move together like synchronized swimmers in a controlled demolition; the more households feel squeezed, the louder the official narrative insists everything is “resilient,” “stable,” and “well anchored.”

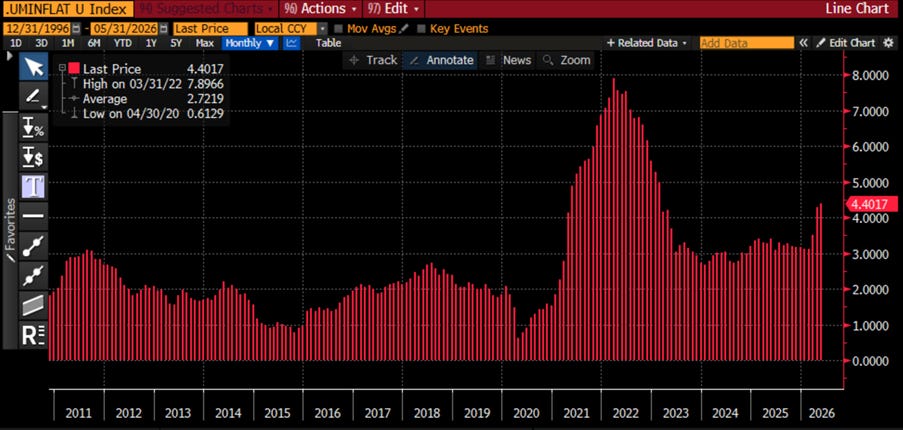

US Umbrella inflation Index (Average of CPI; Core CPI; PPI; Core PPI; Core PCE, 1-year consumer inflation expectations)

Instead of fantasizing about 2% inflation like it’s another campaign bumper sticker, seasoned investors — unlike certain Wall Street strategists still mainlining spreadsheet hopium — can still perform elementary-school arithmetic.

For that miraculous 2% CPI target to materialise by year-end, monthly prints would need to run at below 0.0% from here onward: best of luck engineering that while a freshly politicised Fed chair gets ceremonially crowned and geopolitical conflicts spread faster than a viral TikTok conspiracy thread.

Meanwhile, if monthly CPI keeps printing at a far more realistic 0.2%+, the destination isn’t “price stability” — it’s somewhere between 4.9% and 7.1% CPI by December, complete with complimentary media excuses and emergency talking points delivered with a straight face.

And when reality finally crashes through the narrative, not even Donald Copperfield performing his latest “Central Banker-in-Chief” illusion from beneath a MAGA hat will conceal the fact that cutting rates into an inflationary boom ranked among the Fed’s more spectacular policy magic tricks. Bonus round: every delightful shortage, shipping disruption, and energy shock is lining up with the precision of a choreographed disaster to collide directly with midterm election season — right when voters start asking why their grocery bills now require small-business financing.

Abracadabra: your purchasing power vanished somewhere near the..

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/the-great-war-inflation-tax

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence