The Last Buyer's Club

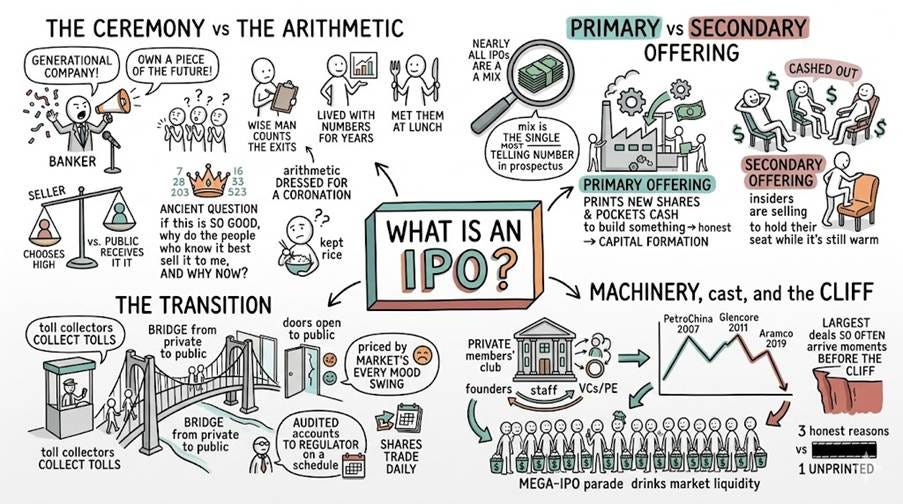

THE MASTER SAYS: when the bell rings, the confetti falls, and the banker on television proclaims that a generational company has arrived and the public may at last “own a piece of the future,” the wise man does not clap — he counts the exits. For an IPO, beneath its silk and ceremony, is but one humble transaction: those who have lived with the numbers for years sell to those who met them at lunch, at a price the sellers chose. This is not wickedness; it is merely arithmetic dressed for a coronation. He who asks, “isn’t this exciting?” has already lost his purse; he who asks, “if this is so good, why do the people who know it best sell it to me, and why now?“ may yet keep his rice. So this issue is a small manual for that ancient question — naming the machinery and the cast, the three honest reasons a company lists and the one it dares not print, how a parade of mega-IPOs quietly drinks the market’s liquidity dry, and why the largest deals in history (PetroChina in 2007, Glencore in 2011, Aramco in 2019) so often arrive moments before the cliff.

An initial public offering is the moment a company stops being a private members’ club — equity locked in the hands of founders, staff and a tight ring of venture and private-equity backers — and throws its doors open to the public, whose shares now trade daily, are priced by the market’s every mood swing, and come with the novel indignity of having to show audited accounts to a regulator on a schedule. It is the bridge from private to public, and as with every bridge, somebody at the booth is collecting tolls. One distinction is worth more than all the confetti: in a primary offering the company prints new shares and pockets the cash to build something — honest capital formation; in a secondary offering, insiders sell shares they already own and pocket the cash themselves, which is the polite term for cashing out and inviting you to hold their seat while it’s still warm. Nearly every IPO mixes the two, and that mix is the single most telling number in the prospectus — which is precisely why the financial press almost never mentions it, and why you should read it first.

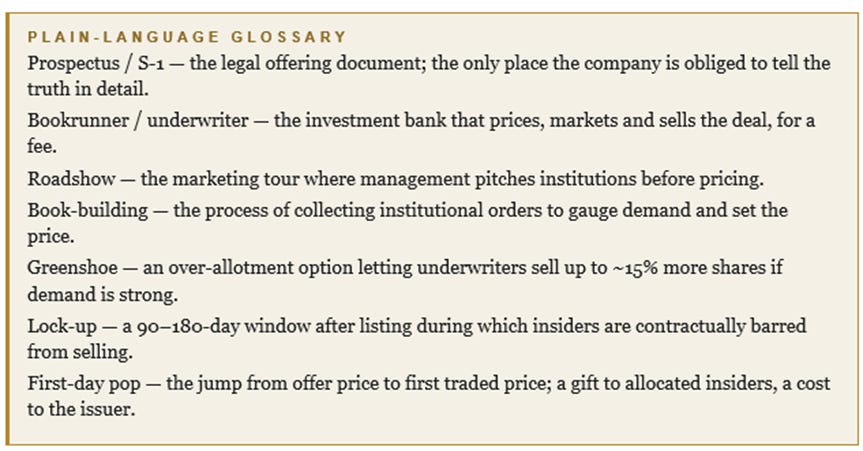

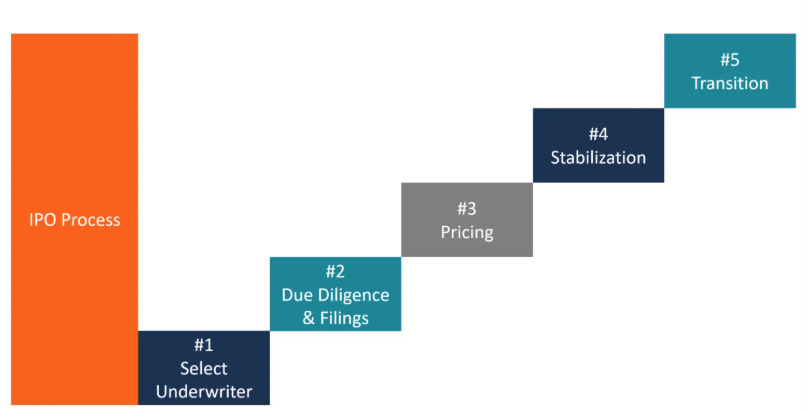

The road to a listing is long, costly and artfully foggy until the last minute, beginning a year or more ahead — supposedly when the company is “ready,” but really when its bankers and backers spy an open window. Underwriters and a syndicate are appointed, lawyers and auditors grind the private books into the giant registration statement (the S-1), a thousand-page tome that buries everything you actually need to know in the risk factors nobody reads. The fashionable move now is to file confidentially first — SpaceX, OpenAI and Anthropic all did in 2026 — so management can rehearse the story before anyone checks the math. Then comes the roadshow: the same slides, the same impossibly large “addressable market,” and the same hockey-stick chart, performed city by city like a touring band with one song, while the underwriters “build the book” and manufacture the evening’s true product — the appearance of scarcity (”ten times oversubscribed!” being a marketing slogan, not an audited fact, and conveniently produced by the very people paid to sell the thing). Pricing happens the night before, set just below what the bankers expect the first trades to fetch, because a day-one “pop” makes lovely headlines and rewards the institutions lucky enough to be allocated — a gift quietly funded by the company itself, which sold too cheap, and by the founders’ dilution. Then the bell rings, the confetti flies, and the lock-up clock starts ticking; three to six months later the insiders are finally free to sell, and that wave of supply is about the most dependable headwind a fresh-faced stock will ever meet.

https://corporatefinanceinstitute.com/resources/equities/ipo-process/

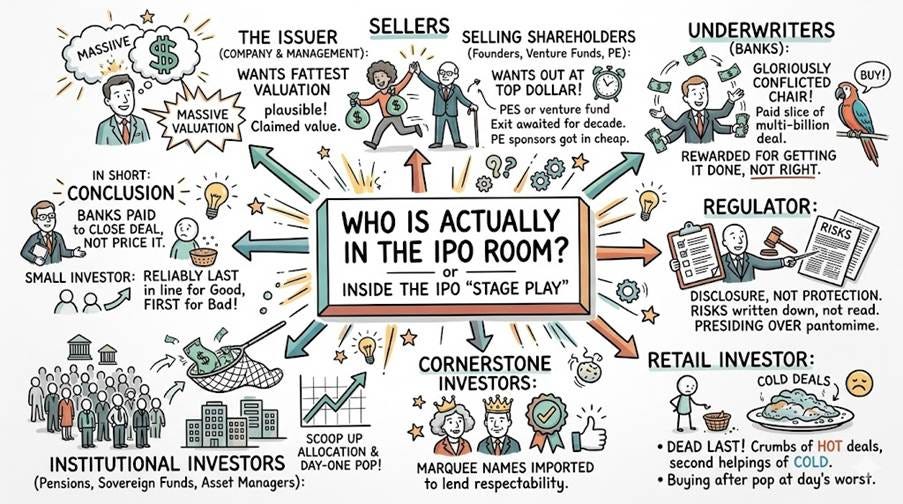

Every IPO is a stage play whose cast is quietly working at cross-purposes. The issuer — the company and its management — wants the fattest valuation it can plausibly claim; the selling shareholders — founders, venture funds wheezing toward the end of their ten-year life, private-equity sponsors who got in cheap — want out at top dollar, the IPO being the exit they’ve awaited for a decade. Those are the sellers. Facing them sit the underwriters, occupying the most gloriously conflicted chair in the building: paid a slice of a multi-billion-dollar deal, they are rewarded for getting it done, not for getting it right — which is why, like clockwork, their research analysts emerge from the quiet period to announce, with a straight face, “Buy.” Behind them queue the institutional investors — pensions, sovereign funds and asset managers who scoop up the allocation and the day-one pop — and the cornerstone investors, marquee names imported to lend respectability. Dead last stands the retail investor, handed crumbs of the hot deals and second helpings of the cold ones, typically buying in the open market after the pop at the day’s worst price. Presiding over the whole pantomime is the regulator, whose job is disclosure, not protection — it makes sure the risks are written down somewhere, not that you ever read them. In short: the banks are paid to close the deal, not to price it, and the small investor is reliably last in line for the good ones and first in line for the bad.

There are three respectable reasons to go public, and we should hear them out before turning cynical, because every so often, they’re true. The first is capital raising: a genuinely growing business needs equity to build factories, fund research or pay down debt, and the public market is the deepest pool of permanent money on earth — a story that holds water whenever the offering is mostly primary and the cash is earmarked for actual bricks rather than someone’s pocket. The second is the cash-out: private stakes are notoriously hard to sell and venture funds tick on a ten-year clock, so the IPO turns paper riches into spendable ones for the early backers — perfectly fair reward for a winning bet, except that when a listing is stuffed with secondary shares and barely a dollar reaches the company, you might gently wonder what the people who know it best can see that the glossy deck cannot, because the quiet exit of the well-informed is never an accident. The third is notoriety and currency: a listing buys legitimacy — a daily price, index membership, analyst coverage and a tidal wave of free publicity — and conjures a tradeable stock that doubles as money for...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/the-last-buyers-club

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence