‘WARSH-INGTON’: A Fed Under Stress

What’s behind the numbers?

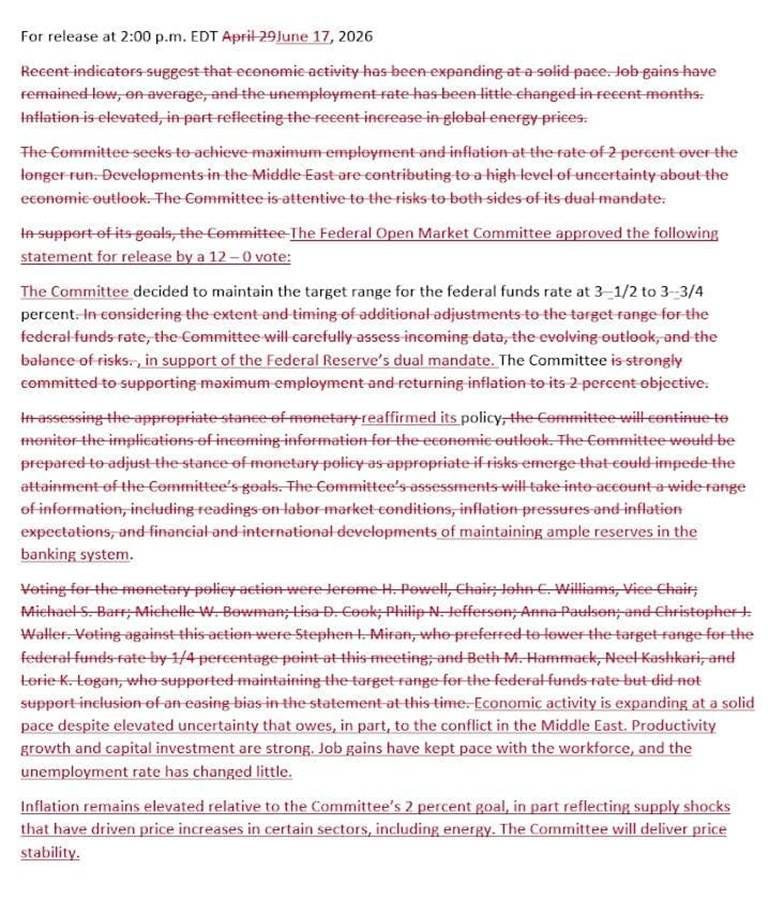

With all the suspense of a magician revealing a card you watched him palm, the Federal Reserve voted unanimously — gasp — to leave rates exactly where they were, parked at 3.5%–3.75% like a car nobody intends to move. Presiding over his maiden FOMC meeting, Kevin “The New Sheriff” Warsh marked the historic occasion not by doing anything, but by saying less about it — heroically taking a pair of scissors to the policy statement and amputating paragraph 4 entirely, because nothing says “regime change” quite like deleting a sentence. So there it is: no forward guidance, no breadcrumbs, no comforting little promise about what comes next. Pillar One of the Warsh Doctrine — talk less — delivered on day one, achieved by the bold expedient of crossing words out. The market, long addicted to being told exactly what to think, now gets to experience the thrilling novelty of not knowing. Mission, technically, accomplished.

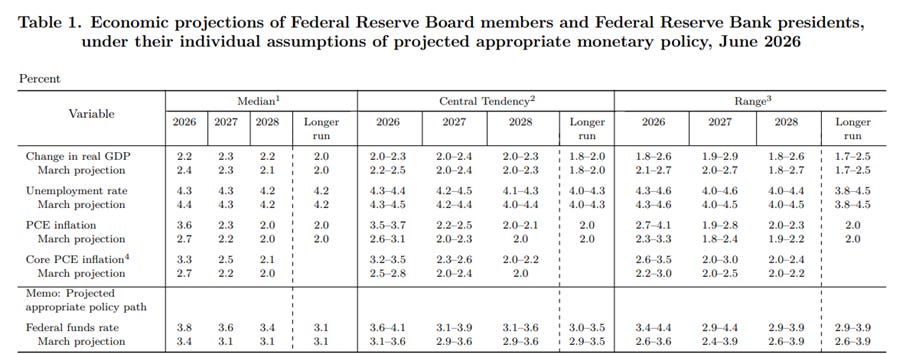

The Fed’s shiny new projections are, to use the technical term, not great. Core PCE is now seen running 3.3% this year — a heroic upgrade from the 2.7% they confidently pencilled in back in March, and suspiciously identical to the latest actual reading, meaning the Fed’s bold forecast for disinflation from here is… none. But fear not: the median dot promises inflation will glide down to 2.5% next year (up from the 2.2% they swore by last time, but who’s counting), growth politely slows, unemployment somehow improves anyway, and core inflation settles at a tidy 2.7% by end-2026 — because in central banking, optimism isn’t a bias, it’s a methodology. The forecast, as ever, remains exactly one revision away from perfection.

The Fed’s beloved “dot plot” — that constellation of anonymous guesses dressed up as policy — has staged a dramatic about-face, quietly burying the easing bias of the Powell era under a fresh pile of hawkish ambition. Where the prior Fed had zero officials forecasting hikes this year, suddenly nine of them have discovered a sudden enthusiasm for raising rates: three dots leaping to two hikes, a brave soul pencilling in three, and the entire dovish wing — the seven who wanted a cut, the two who wanted two, the lone four-cut dreamer (a fond farewell to Stephen Miran’s optimism) — evaporating almost entirely, leaving exactly one cut-hopeful clinging on. In other words, the committee that spent last quarter eyeing the exit now eyes the brake pedal. The cherry on top: only 18 of 19 officials bothered to submit a dot at all, with speculation that the missing contributor was none other than Warsh himself — the man who thinks forward guidance is a confusing crutch declining, with exquisite consistency, to add his own dot to the guidance chart he’d love to abolish. Enjoy the dot plot while it lasts. Under a Chair who’d happily feed it to the shredder, this may well be one of its final appearances.

Kevin Warsh strode to his first podium as Fed Chair and delivered the monetary policy equivalent of a fortune cookie — fewer words, fewer forecasts, fewer clues, and a statement so stripped-down it made Hemingway look verbose. “Just the facts,” he declared, abolishing forward guidance on the grounds it was “not well suited” to current circumstances, which is central banker for “we have no idea what’s coming and would rather not be held to anything.” The irony, apparently lost on no one except Warsh, is that a communications vacuum doesn’t produce silence — it produces nineteen regional Fed presidents suddenly discovering they have opinions, each one gleefully filling the guidance gap with their own flavour of Fed-speak. Meanwhile, on the balance sheet, he solemnly reaffirmed ample reserves — translation: nothing is changing yet, despite years of thundering rhetoric about the $6.7 trillion blob — while announcing four shiny new task forces covering communications, the balance sheet, data sources, and productivity, because nothing says “regime change” quite like forming a committee to study the possibility of eventually planning some change. He did, however, repeat twice that “inflation is a choice“ and that this committee will “deliver price stability“ — notably without once mentioning the employment half of the dual mandate he swore to uphold at his swearing-in three weeks ago. So: less talk, more task forces, and a mandate that already appears to have quietly lost a leg. Day one in the books.

FED Balance Sheet since 1995.

Thoughts.

While Wall Street and The Manipulator In Chief continue their favorite magic trick—convincing investors that the Federal Reserve can steer the business cycle—the reality is less enchanting: in every inflationary bust driven by rising oil prices, the Fed has historically been forced to raise rates, not cut them.

FED Fund Rate (purple line); S&P 500 Index to Oil ratio (green line); 7-Year Moving Average of S&P 500 Index to Oil ratio (red line).

On 22 May 2026, Kevin Warsh swore an oath, shook some hands, and inherited the worst job in finance: running a central bank that the President wants to boss around, an economy doing its best impression of the 1970s, and a mandate he’s promised to rip up and rebuild. The 17th Fed Chair walks in just as inflation walks back. This edition is your field guide to what actually changes when the Chair changes — for the rulebook, for the four asset classes your portfolio cannot escape, and for the Fed’s most delicate possession of all: its independence, currently being stress-tested in public like a bank that forgot to hold capital.

https://www.reuters.com/business/warsh-takes-over-fed-with-policy-problem-already-view-2026-05-22/

Power at the Fed doesn’t change hands like power at a company — there’s no founder’s farewell, no succession plan in a charter, just one of seven Governors who happens to set the weather for the other six. On paper the Chair is first among equals; in practice he frames the debate, controls the microphone, and decides which fires to fight and which to let burn. So, when the Chair changes, the regime changes — same dual mandate, same statute, same marble building on Constitution Avenue, entirely new forecast. And Kevin Warsh did not arrive whispering “steady as she goes.” He arrived promising “regime change,” musing aloud about resetting the institution and, at one charming moment, breaking a few heads — before discovering that the people whose heads were on the list still had to show up to work. The complication is that three forces hit Warsh on day one, each pulling a different way: a President who hand-picked him and would like his rate cuts now, please; an oil shock and resurgent inflation that rudely deleted the cozy disinflation he was hired into; and Warsh’s own genuinely held, deeply unfashionable convictions about balance sheets, central-bank chatter, and what inflation even is. Three vectors, three directions, one Chair in the middle. That collision is the next four years.

https://truthsocial.com/@realDonaldTrump/posts/115983891481988557

Here’s a fact that should detonate every solemn debate about Fed independence: the Fed wasn’t born independent at all. When Woodrow Wilson signed the Federal Reserve Act on 23 December 1913 — after decades of bank panics convinced Washington it needed an elastic currency and a lender of last resort — the new central bank came with the Treasury Secretary bolted directly onto it. Under the 1913 Act, the Secretary of the Treasury and the Comptroller of the Currency sat on the board by virtue of their day jobs, and the Treasury Secretary was its ex-officio Chairman. Translation: America’s first central-bank chief was a sitting Cabinet officer who answered to the President — the very arrangement we now clutch our pearls about. The sacred wall between the Fed and the White House wasn’t a founding feature; it was a renovation. It took the Great Depression and Marriner Eccles to do the remodelling: the Banking Act of 1935 evicted the Treasury Secretary and the Comptroller, built the modern FOMC, and created a proper Chairman drawn from the Governors. So the independence Warsh’s tenure is about to stress-test isn’t some ancient birthright — it’s a hard-won patch installed after the Fed spent its first two decades demonstrating exactly why you don’t let the Treasury chair the central bank.

https://www.federalreservehistory.org/essays/federal-reserve-act-signed

Installing a Fed Chair is a deliberately bureaucratic obstacle course, and that’s the whole point. The seven Governors are nominated by the President and confirmed by the Senate for a single, non-renewable fourteen-year term, staggered so one expires every two years — a clock so long and so slow that no President is supposed to be able to stack the board in one go. From that pool, the President anoints a Chairman and Vice Chairman for renewable four-year terms, Senate permitting. And here’s the kicker that just bit everyone: when a Chair’s four years lapse, he doesn’t have to leave — he can squat on his Governor’s seat for the rest of those fourteen years.

https://www.stlouisfed.org/in-plain-english/federal-reserve-board-of-governors

Warsh’s ascent ran this exact gauntlet and rattled every bolt in it: confirmed to the Board on 12 May 2026 and as Chairman on 13 May by a 54–45 vote so partisan it set a record for divisiveness, then sworn in on 22 May to replace Jerome Powell. Powell, in turn, declined to ride off into the sunset — his chairmanship expired, but he kept his Governor’s chair, a polite reminder that the fourteen-year clock, not the President’s mood, decides when a Governor goes home. That gap — four years for the Chair, fourteen for the seat — is precisely where central-bank independence lives or dies. The upshot frames everything: a President can pick the Chair but can’t empty the room around him, and a Chair can set the mood music but can’t dictate the...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/warsh-ington-a-fed-under-stress

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence