Eternal Bullion…

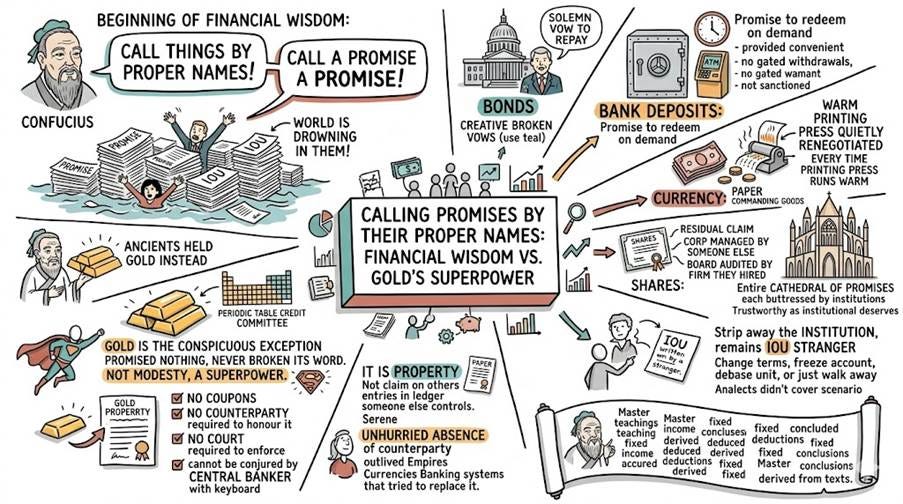

Confucius once observed that the beginning of wisdom is to call things by their proper names. The beginning of financial wisdom is to call a promise a promise — and then to notice that the world is drowning in them. Every financial asset that men have invented is, at its dignified core, a promise.

A bond is a government’s solemn vow to repay — the kind of vow that governments make with great ceremony and break with even greater creativity.

A bank deposit is a promise to redeem on demand, redeemable at any hour of the day, provided the hour is not inconvenient, the bank has not gated withdrawals, and you have not been sanctioned.

A currency is a promise that the paper in your hand will still command goods tomorrow — a promise renewed daily, like a marriage of convenience, and quietly renegotiated every time the printing press runs warm.

A share is a promise of a residual claim on a corporation managed by someone else, governed by a board you did not choose, audited by a firm they hired themselves.

The Master taught that a man of honour keeps his word. Modern finance has instead built an entire cathedral of promises, each buttressed by the institution that issued it, each only as trustworthy as that institution deserves to be — which is to say, some very trustworthy and some, shall we say, aspirationally trustworthy. Strip away the institution and what remains is an IOU written by a stranger who may change the terms, freeze the account, debase the unit, or simply walk away to pursue other opportunities. The Analects do not cover this scenario. They did not need to; the ancients held gold instead.

Gold is the conspicuous exception — the one major asset that promised nothing in the first place and has therefore never broken its word. This is not modesty. It is a superpower. Gold does not pay a coupon. It does not require a counterparty to honour it. It does not need a court to enforce it. It cannot be conjured into existence by a central banker with a keyboard and a mandate to be creative. It is property — not a claim on someone else, not a favour owed, not an entry in a ledger that someone else controls. That single quality — the serene, unhurried absence of a counterparty — is the reason gold has outlived every empire, every currency, and every banking system that has ever tried to replace it. As the Master might have said, had he worked in fixed income: He who trusts no one cannot be betrayed. He who owns gold trusts no one. Draw your own conclusions.

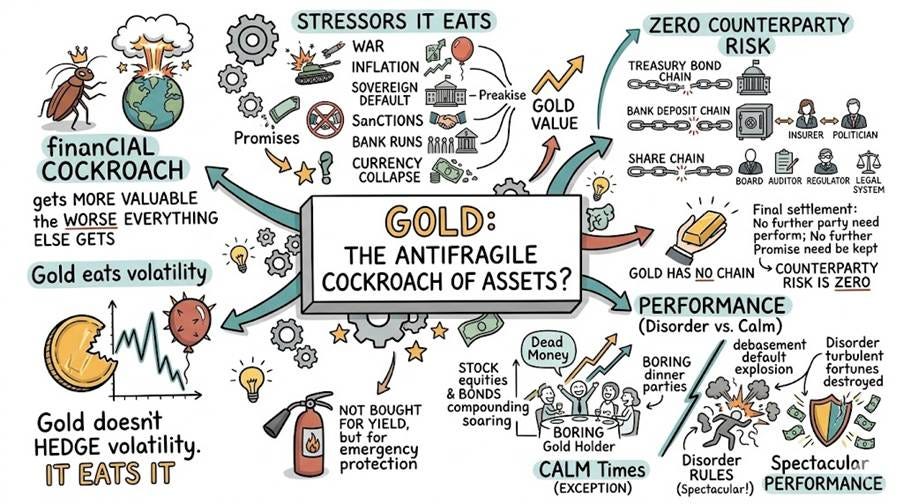

Gold did not survive three thousand years because it is shiny. Many things are shiny. Politicians’ promises are shiny. Leveraged structured products were, briefly, very shiny indeed. Gold survived because it is the only money that no one can default on — the only financial instrument whose credit committee is the periodic table

Nassim Taleb gave us “antifragile“ to describe things that don’t merely survive chaos but grow fat on it. A wine glass is fragile. A paperweight is robust. An antifragile asset is the thing that gets more valuable the worse everything else gets — the financial equivalent of the cockroach that inherits the earth after the nuclear exchange. Gold is that cockroach. War, inflation, sovereign default, sanctions, bank runs, currency collapse: every one of these is a stressor that destroys the value of promises and increases the value of the one asset that isn’t one. Gold doesn’t hedge volatility. It eats it.

The mechanism is counterparty risk — or rather, its total, glorious absence. A Treasury bond chains your wealth to the continued solvency, honesty, and goodwill of the issuing government. A bank deposit chains it to the bank, the deposit insurer, and the political will to honour the scheme when honouring it becomes inconvenient. A share chains it to a board, an auditor, a regulator, and a legal system that will theoretically enforce your claim — eventually, after fees. Every one of these is a chain, and a chain breaks at its weakest link. Gold has no chain. An ounce in your hand is the final settlement: no further party need perform; no further promise need be kept. In the language of risk management, its counterparty risk is zero. In plain language, it’s the asset you hold when you’ve decided to stop trusting strangers with your money.

And yes — over a calm times, gold looks like dead money. It yields nothing while bonds compound and equities soar and everyone at dinner parties tells you how boring you are. But calm decades are the exception in monetary history, not the rule. The rule is debasement, default, and disorder, occasionally interrupted by stretches of stability long enough to make people forget the rule. Gold does poorly in the stability. It does spectacularly in the disorder — and since the disorder is precisely when fortunes are destroyed, the insurance is worth rather more than its average annual return implies. You do not, after all, buy a fire extinguisher for its yield.

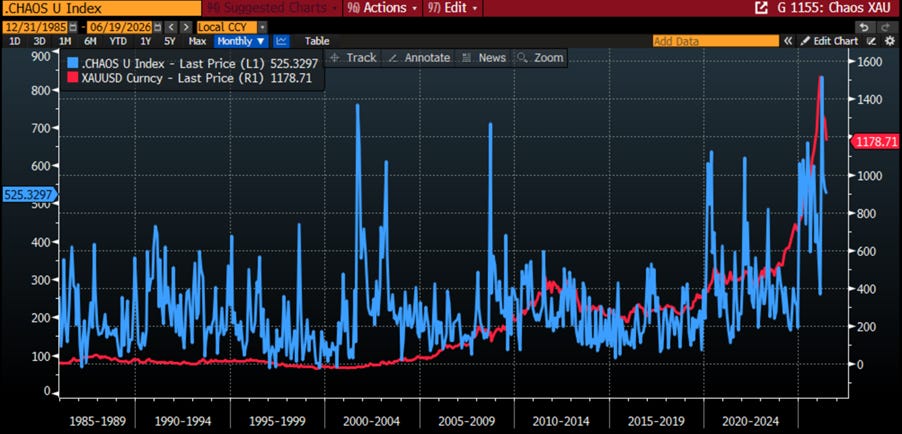

US Aggregate Chaos Index (blue line); Gold Price in USD (red line).

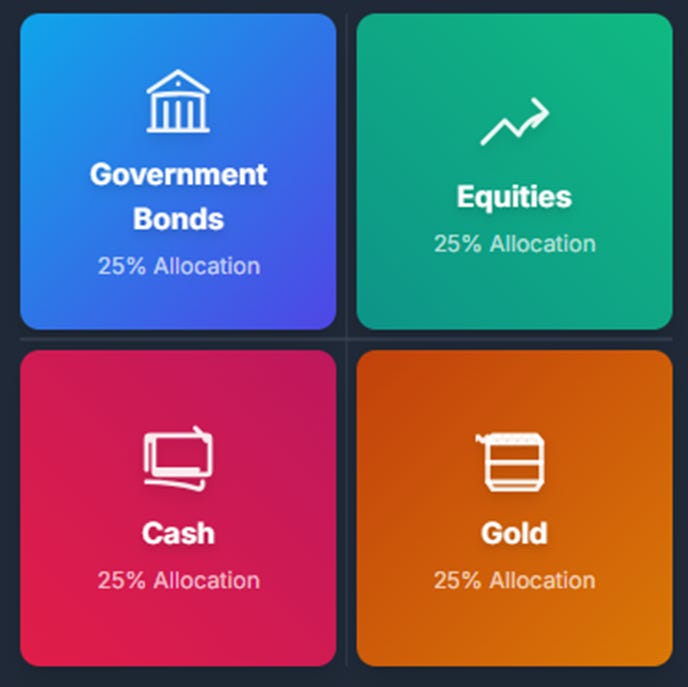

Harry Browne’s Permanent Portfolio — stocks, bonds, cash, gold, one equal slice each — is a fine framework, but there is a simpler cut: forget the four seasons and draw one line instead, the line between contracts and property.

On the left sit the contracts — bonds, cash — which are not really things at all but politely worded IOUs from public institutions, worth precisely as much as those institutions deserve to be trusted, which on a good day is quite a lot and on a bad day is the subject of this newsletter.

On the right sit the property — equities and precious metals — which are ownership of actual, physical, stubbornly real things that continue to exist regardless of what any government decides, prints, freezes, or tweets at 2am. The central insight is this: when the world trusts its institutions, capital migrates left toward the contracts; when it stops, capital migrates right toward the property. Everything that follows in this letter is simply an argument that the migration is already underway — and that gold, the most property-like property of all, is its principal destination.

When trust in public institutions rises, capital migrates toward contracts — people happily lend to the state, hold its currency, and pocket its promises, secure in the belief that the cheque will not bounce. When trust falls, capital moves the other way: out of bonds and cash, into equities and precious metals, from the public side of the ledger to the private one, from claims on institutions to ownership of things. The great wealth-preservation question of our age is therefore not “will there be inflation?” or “where are rates going?” — entertaining as those parlour games are — but the rather more uncomfortable one: do you still trust the institutions whose promises fill your portfolio? For a growing share of the world’s investors and central banks, the honest answer, delivered quietly and in tonnages of gold, is...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/eternal-bullion

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence