Doomberg: Why energy abundance may be ahead

In this episode, Doomberg argues that many of today’s assumptions about energy scarcity, geopolitical power, and commodity markets are being tested in real time.

While conflict in the Middle East has dominated headlines, he sees a different story emerging beneath the surface: one of resilient energy markets, abundant hydrocarbon resources, and a world gradually adapting to disruptions that once would have sparked crisis.

At the same time, shifting global alliances and growing interest in gold as a neutral reserve asset may signal deeper changes in the international monetary order.

Watch the episode now.

Transcript

Doomberg

Iran and Israel have traded projectiles. Trump is on Truth Social claiming that Iran shot down a US helicopter and the military needs to, quote, do something about it. The war in Iran has demonstrated to the world definitively that the era of unipolarity is over. The US military is not the dominant force it used to be that could project debilitating power for extended periods of times across all four corners of the globe.

Very few people would have predicted at the beginning of this war that we’d be 100 days into it and Iran will have successfully fought the vaunted power of the the US and Israeli militaries combined to a standstill. They would say they’ve done better than that. I’m being generous. And so here we are, that momentum has stalled. The détente that Iran has been able to achieve has laid bare the weakness of the US military compared to perceptions.

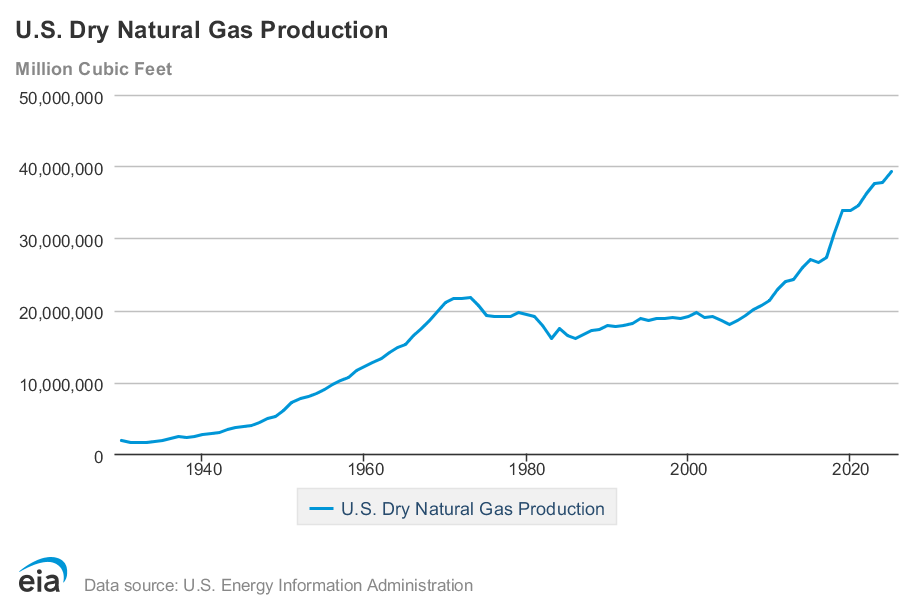

I do think Trump in the back of his mind knows this, needs to get this war in Iran wrapped up. The oil market will be changed forever because of this, not in a bullish way. And then what do you have is a world awash in natural gas and natural gas that has come out of it way better than expectations. So here we are.

Monetary Metals

Welcome back to The Gold Exchange Podcast. I’m joined by my favorite green chicken, and that is the head writer of the Doomberg Substack. Doomberg, welcome back to the show. It’s been a crazy time in the energy markets and we have not had a guest more requested than yourself. So welcome back to the Gold Exchange Podcast.

Doomberg

Well, I’ll bet when you’re a, you know, one of a set of one, what can I tell you? You know, it’s great to be back with you.

What’s going on in the oil market?

Monetary Metals

We’re very excited to have you on. I wanted to talk about the oil markets. Obviously, there’s been so much volatility. Prices have gone up, then there’s been a tweet or a truth post, then they’ve gone down. People are saying soon there’ll be $150 oil. The oil market isn’t pricing something in, but I wanted to talk to an expert who knows really almost more about the oil market than really anyone.

What is going on in the oil market? Is market pricing really what we should be focusing on and saying, hey, if the market says this is the price, we got to kind of take that as our main source of truth. Or is there something that most people are missing when they’re analyzing this market?

Doomberg

Yeah, it’s a great question. It’s obviously the question of the times for energy analysts. I think to answer your question upfront, I think all pursuits of the truth have to start with the market as your foundational axiom. Money is being wagered. Experts are expressing their opinions through the most visceral way possible, which is in the form of their hard-earned savings or the savings of the people they’re investing on behalf of. And very early on in this war, we were quick to confess

Others have been slow to realize that everybody got it wrong. I don’t think anybody given this fact set would have assumed that the price action we have observed would’ve been their base case. And what have we gotten wrong? Oil did not, did not even reach the highs seen during the early weeks of the war in Ukraine, which comparatively was a much smaller disruption to the oil markets.

And so when we saw what oil was doing and more importantly what it wasn’t doing, we immediately said, okay, we’ve got something foundationally wrong.

Let’s go on a journey to try to figure out what that might be. And one of the more interesting observations observations is that there’s a whole genre of people who frankly I think should know better, who are kind of, as we’ve said in other podcasts, like standing on the front lawn, old man shaking their fist at the neighbor’s kids.

Like the market is wrong, the market is missing something. Next week we’re going to 150. And even today, like, you know, Iran and Israel have traded projectiles. Trump is on Truth Social claiming that Iran shot down a US helicopter and the military needs to quote, do something about it. And as we’re talking, WTI is down what? Let me just pull it up.

Yeah, it’s only down $4 to $87 a barrel. So again, this tells you that the foundational axiom is incorrect. And so what has transpired? Well, to be totally transparent, the same group of people, including us, who got it so wrong, are now trying to figure out why. Perhaps you should take what we say with a grain of salt, but the coalescence of opinion is centering upon the fact that Chinese were far better stocked for this war than people had anticipated.

We had alluded to China stockpiling oil and other war-related commodities in piece we wrote last year called War Rations. And, and people assume the, the Chinese were buying 500,000 or 750,000 barrels of oil a day extra versus what they needed, but clearly they were doing much more than that.

They have been able to cut their imports by 4 or 5 million barrels a day without seemingly missing a beat. And then the circumvention of the Strait of Hormuz has been initially more effective, and as time goes on, progressively more effective, which I think plays into Trump’s hands a little bit because we suspect the Iranians were hoping that the Strait of Hormuz being closed would cause a quicker and more violent economic calamity than has unfolded.

So in a way, the Chinese are helping Trump and hurting Iran in this regard. And so as oil continues to trade sub-$90 a barrel and settles on the new reality that certain poor consumers around the world are just going to do without while the rest of the world pays somewhat more than they were paying before the war and new supplies are brought on stream and substitutions are made and all that jazz.

Absent a complete destruction of all the assets in the Middle East, which we’re always very careful to say is a possibility and one that would be a true calamity, we think that the oil market will be changed forever because of this and not in a bullish way. So that’s a bit of a probably more comprehensive answer than you were looking for, but that’s our state of thinking today.

Monetary Metals

And can talk to us about this kind of disconnect between the resiliency of the oil market going forward and current prices. Like you mentioned, if someone were to have given you this fact set prior to the events unfolding, you would say, well, maybe $150 oil or, you know, definitely sub $90 oil would be quite surprising. So why is there this disconnect between maybe the disruptions in the oil market and the oil prices? But maybe more importantly, What does that mean for oil and energy as an asset class where if this level of event is happening and $100 oil is not being broken, what does that mean for the asset class going forward?

Doomberg

Well, that’s kind of the argument we’ve been making. I mean, if you can’t get $150 oil with this fact set, I mean, I guess if you think the Saudi oil fields are going to get blown up and then sure, as an insurance policy, buy a few out-of-the-money call options, but it can’t be your base case anymore. Our view longstanding is that the long-term real price of all commodities is lower and that which doesn’t kill you makes you stronger.

Longer, to like borrow a cliché, what we’re seeing is the sort of free market responding to scar tissue in a way that, you know, makes it more resilient. And so in a way, the war in Ukraine caused everyone perhaps to get a little bit more resilient to energy shortages. And then this time around, those who were a little late to that game, even the progressive government in Australia is coming around to the fact that maybe physical possession of one’s emergency stocks is a better idea than a paper commitment from the US Gulf Coast.

And so what does this mean long-term? There’s just an awful lot of oil. And when we look across the board, you know, we have this evolution towards lighter hydrocarbons that we have been flagging for some time, both in our articles and in our Doom Zoom Pro Tier presentations.

Natural gas in the US is trading for $18 a barrel oil on an energy equivalent basis. There’s an enormous amount of it everywhere, you know, a major multinational oil and gas company looks, they trip over hundreds of, you know, TCFs of natural gas sitting underground. And as oil becomes scarce and as oil becomes artificially held higher in price because a cartel’s in the middle of it or a war in the Middle East has broken out, that just accelerates the engine switching and other substitutions, renewables at the margin, pick your favorite. And that makes the overall energy complex more resilient.

And it, of course, in hindsight, it all makes perfect sense. And I, again, I don’t want to pretend as though like this wasn’t a surprise to us. It certainly was. But when you look at the Statistical Review of World Energy, which is sort of our Bible for unbiased data, and you plot global human energy consumption over the last 60 years, it’s a straight line up and to the right. Yes, there’s a blip for COVID, and yes, there’s a blip for the global financial crisis, and yes, you can squint and see where the Arab oil embargo was, but the human endeavor is the consumption of ever more energy at lower and lower real prices.

The single greatest bet of a lifetime that there will be more energy consumed by humans and it will cost less. And so I don’t know how you get to 150 in today’s dollars, ever. I mean, again, absent a complete destruction of those assets, and it doesn’t seem as though this is something Trump is courting.

If anything, he seems to be trying to end the war, for which we would give him credit. And so as long as things don’t go crazy, what comes out of this war is the world realizes that maybe a million barrels a day isn’t as inelastic as it used to be, let alone 5 or 10 million barrels a day. And who knows, it’s going to be a fascinating world.

Oil vs gold: Why are they moving differently?

Monetary Metals

And I want to ask you now, contrasting two asset classes here, one is this kind of oil and energy market, the other is the gold market. I think both of us can see a world, and we recently saw a world where gold was hitting all-time highs, and maybe that was even without some, you know, crisis events, a monetary reset, or any kind of major conspiracy event where, oh, the BRICS countries are launching a new gold product.

Basically, people said, well, you know, with inflation and kind of this global supply chain disruption, maybe some stagflation around the people thought, I’m going to add to my gold positions, pushing gold prices higher, central banks loading up on gold, but no major kind of flashpoint or crisis. And yet a major flashpoint and crisis happening in the oil market, and we don’t see oil prices hitting an all-time high.

So do you think that there is similarities between these asset classes, or do you think that maybe this year, 2026, is where we see, no, this is why gold reacts as an asset class in this way and maybe has a different future than oil as an asset class or the energy market going forward?

Doomberg

So oil and gold are wildly different things. Gold is an inert metal with 5,000 years of history of representing money. Oil is a consumable that is desperately needed for the human endeavor, which is a constant unrelenting struggle against the forces of entropy. You have to waste heat in order to impose order on your local environment. In other words, to have a high standard of living. And the stock-to-flow ratio of gold is just vastly different than oil.

.And what I think we’re seeing with this medium-term weakness in gold gold since the war broke out. And we have a very simple mental model for this. Like, why is war risk and gold trading inverse to each other? All of the countries on the wrong side of the strait owned a lot of two things when the war started.

They owned a lot of gold and they owned a lot of oil, and they can’t sell their oil and they have to sell something. And so as the war drags on, I just think that they’re selling their oil. And so I own a lot of gold. Hasn’t been fun. I don’t plan to sell my gold and I’ll just sort dollars cost average in with my various investments over time.

Hopefully the doom bucks keep flowing in and I can peel off a few of them to add to my ounces total. Not to sound like a Bitcoin maxi or anything, but I do think until the war is resolved, it’s going to be difficult for gold to appreciate in US dollar terms. I don’t like to say gold going up or gold going down because in my view it’s sort of the reverse. The global fiat currencies are measured against gold. How many ounces of gold can a fiat currency buy?

It’s been that way forever. The last 60 or 50, 60 years have been a perversion of that. But ultimately, I do think that’s what the post-war world looks like, and that’s why I’m quite bullish gold in the aftermath of this, because ultimately the war in Iran has demonstrated to the world definitively— it’s not how you’ll read it in the Western media, but it has demonstrated to the world that the era of unipolarity is over. The US military is not the dominant force it used to be that could project debilitating power for extended periods of times across all four corners of the globe.

Very few people would’ve predicted at the beginning of this war that we, we’d be 100 days into it and Iran will have successfully fought the vaunted power of the US and Israeli militaries combined to a standstill. They would say they’ve done better than that. I’m being generous. So here we are.

Monetary Metals

And back to this kind of oil versus gold thought process. Obviously, you know, we’re discussing gold as a monetary asset and has this kind of monetary flavor with a stock-to-flow ratio. Versus a consumable like oil. Can you talk to us about this idea of this strategic petroleum reserve where countries said, hey, we got to get some oil just in case something bad were to happen versus, you know, gold as a reserve asset?

Do you kind of see those similarly where they say, hey, in times of crisis, let’s have an immediately liquid and usable asset, whether that’s oil or gold? And do you think that’s going to change going forward with this kind of idea of energy abundance versus something like monetary abundance where people are saying, Do I really want more fiat currency or do I want more gold versus we’ve got lots of oil? Do we really need a strategic petroleum reserve?

Doomberg

So it’s a great question. It very much depends on which country you’re in. So it’s probably worth doing a bit of a historical sort of telling of how we got to this situation. So they’re twin issues. So when Nixon removed the US off the gold window and then you had the war in the Middle East back then, the Arab oil embargo ensued.

And what was born out of that was the IEA, the International Energy Agency, and the mission of the IEA was to protect the developed world, the oil importing countries at that time, from such supply shocks by mandating that all of the member states of the IEA held 90 days of oil or refined products in inventory at the ready for just such an eventuality. It was a twinning of the gold and oil stories in a way that is like echoing today in this war in the Middle East.

Now, the US at the time was the world’s largest importer of crude. Now you fast forward to today where 15 years into the shale revolution and the US is not actually an importer of crude net. We’ve addressed this. There’s a bunch of nonsense floating around on Twitter trying to argue that the US is somehow not an energy superpower.

It’s just, I’ll catch myself before I say something I regret. So the US actually doesn’t need a strategic petroleum reserve, but it has one. It’s a big one. And what it has done, again, I give credit to my good friend Sir JJ over at Market Fives. Jack Johnson writes a great Substack twice a day. Can’t recommend it enough. He pointed out, I think quite cleverly, that the US is not draining its strategic Federal Reserve right now, it has lent oil to Exxon and Chevron who are to pay back that oil with interest, not in dollars, but in barrels.

And so all of the oil being lent to the market right now for the exact purpose of managing the crisis is to be paid back. And the credit of the people borrowing is just as good as US Treasuries. In other words, Exxon’s corporate credit rating is incredible. And so the oil is still there. It’s just in the form of future deliveries where the person standing on the other side of your transaction is Exxon or Chevron or pick favorite.

And viewed through that lens, I think the collective working capital of oil sitting around the world has now pivoted from being viewed as an efficiency drag to a resilience boon because the value saved by shaving off the marginal price spike is integrated across the entire transaction suite.

And so coming out of this crisis, I don’t imagine any country in the world is going to say, I’m going to take a few months to top off my stores. Like they’re not, as if they’re not going to say that now. And so Australia is not going to be caught with 30 days again and the US will refill its strategic reserves. It’s already got the legal mechanism in place for that to happen organically.

And every other country in the world is going to look around and say, you know, as oil slips back down to 70 and 65 and 50 and 40, which is coming, maybe we’ll go in and that slope will be buffered a bit by this investment in resiliency that these stores bring. And then what do you have? What you have is a world awash in natural gas and natural gas Metals Liquids that has run through the gauntlet of the closure of the Strait of Hormuz and come out of it way better than expectations. And, um, lower for longer, consistent with our long-term view that all shortages are followed by gluts.

Venezuela, Guyana, and The New World’s oil

Monetary Metals

Doomberg, I got to say, it’s always fascinating having you on the podcast, but your last answer actually proved my last video wrong. I did an oil versus gold video explaining the differences between oil and gold, and I said that unlike gold, you can earn a yield on gold paid not in dollars but in more ounces of gold.

That’s not true of the oil market, but it turns out I’ve been proven wrong on this podcast. Oil can actually be loaned and paid back in more barrels of oil. Very fascinating. And I want to ask you a question about these oil companies. We’ve heard this idea that, well, a lot of these oil companies, they wanted to get oil out of Venezuela because Venezuela had all this great oil reserves.

They pushed out these U.S. and Western oil companies. Now that the U.S. is kind of more strategically involved in Venezuela, if you want to call it that, these oil companies are now going to start refining and producing oil from Venezuela. How true is that idea and how important is that Venezuelan oil to America’s oil independence?

Doomberg

Yeah, so before I do that, I just want to close the loop on this loaning of barrels. The best part of it all is that the president and his administration could do this without congressional involvement because there’s no dollars changing hands, only barrels. And so it’s not an appropriation or any sort of congressional oversight at all. And look, when you have Scott Bessin and Chris Wright in the seats of Treasury and Energy respectively, then, you know, you have two people who know far better than you and I what they’re doing.

So to your question on Venezuela, Venezuela’s an interesting one. We just did a full deep dive analysis on Guyana for our May Doom Zoom, and I don’t think that the Guyana story is independent of what’s been going on in Venezuela. So Exxon discovers a generational asset offshore in Guyana, really one of the most remarkable finds of this sort of generation from zero to a million barrels a day almost in a matter of less than a decade, which is just unheard of and for one, you know, bloc. And Exxon had been kicked out of Venezuela. Chevron stuck around. You have the armada of super majors assembling offshore in Guyana.

Venezuela’s then leader, president, dictator, pick your favorite adjective, Nicolás Maduro was agitating to resuscitate a century-old border claim against Guyana that would have then enveloped the offshore assets of Exxon into Venezuela. And then next thing you know, total coincidence, US military snatches him The US is back in Venezuela. Color us skeptical, but we first wrote about the prospects of all of this back in a piece we wrote in December of 2023 called The New World’s Oil, foreshadowing the Monroe Doctrine.

So when you look at northeastern coast of South America, you have Venezuela, Trinidad and Tobago offshore, Guyana next door, Suriname next to that. There’s 5, 6 million barrels a day of oil to be had there. Easily. Venezuela used to produce 4. It was doing less than 1 before the events of early January. You have Trinidad and Tobago, which is a natural gas powerhouse right there offshore. You then have Exxon next door in Guyana. They’ll probably get that to 2, 3 million barrels a day, an enormous amount of natural gas. Surinam next door, right on the edge of Guyana. So just there, forget about the, the rest of the southern part of the Western Hemisphere.

And then you mix in the fact that Venezuela’s oil oil is heavy, similar consistency, you know, gravity, sulfur content to that of Western Canada in Alberta, and that US refineries are optimized to run such grades. And the fact that the oil being produced in the Permian and the other shale regions in the US is much lighter, the synergistic combinations of the two makes for an ideal slate for refining in the US.

And it all just kind of makes sense. And that’s why the war in Iran is such a mystery to us and such own goal/catastrophic mistake by Trump. The Western Hemisphere in the New World’s oil, we estimated, you know, from the southern tip of Argentina to the Arctic has an extra 10-12 million barrels a day of oil to be had and an infinite amount of natural gas. Like, what are we doing in the Middle East? Let China figure that out. But anyway, I digress.

China’s secret oil stockpile and gold strategy

Monetary Metals

And let’s talk about the China situation. Obviously, a lot of people said, wow, China is so dependent on these oil imports from the Middle East. We haven’t seen a major breakdown in the Chinese economy, at least from official numbers. What’s your take on what’s what’s actually going on in China? Was it really that they had a glut of energy that they didn’t tell anyone about?

And do you think that there are similarities with the gold story, which is a lot of people have said, oh, China’s adding all these gold reserves in secret, they mine all this gold, they’re the number one mining of gold country in the world, and yet no gold is really flowing out of China? So where do you take the oil kind of conspiracy, and do you map that onto gold in any similar way?

Doomberg

Oh, I think China has been preparing, and I give full credit again to— when I read things other people create and produce and believe it, I like to give them credit. You know, I’ve been reading Luke Gromen for a long time. I’m sure you know Luke. China is positioning for a world where gold is the neutral reserve asset for the settlement of imbalances in international trade. So let’s take a step back and divide it into China or energy, China gold. So China energy, we’re going to do a Doom Zoom next month, an updated look at China through the lens of energy.

Look, China’s a coal story first and foremost, a domestic coal story. Half its primary energy comes from coal. It’s a hydro story. It’s a nuclear story. It is somewhat of a solar and wind story, although we are putting out a piece later this week sort of cutting through that nonsense. Crude oil’s important, less so, obviously has huge amounts of crude oil that it has been importing quietly for the past few years. And I’ve seen estimates of 1.8 billion barrels. It has insulated itself from the weaponization of the Middle East, and it’s standing there unperturbed.

Credit is due. I think that’s quite the strategic coup on the part of the Chinese leaders. Once this war is over and crude becomes widely available and less expensive, who’s the winner? China. China bought cheap, sold high, and then buys cheap again. It’s like the trade of a lifetime. And then now separately on gold, I think the Russians and the Chinese have been collaborating since 2014, which is when we have pegged that World War III started.

We don’t think that Russia selling down its treasuries and China opening up the Shanghai Physical Gold Exchange are coincidences. All of this flowed in the aftermath of the 2014 Ukraine affair and Putin’s move on Crimea and Georgia and the subsequent US sanctions against Russia, which kind of shocked everybody. We’ve not yet written this up. I’ve talked about it on a few podcasts. Russia and China were co-victors of World War II with the US. They were given veto at the United Nations Security Council, which was supposed to be the place where sanctions were conceived and voted on. And the possession of a veto was meant to ensure that none of the P5 members were ever sanctioned.

P5 being, you know, the three I just mentioned, and then Great Britain and France as proxies for the US. And so the, the sanctioning of Russia en masse after 2014, I think was a real eye-opener to the other P5 members, China and Russia. And they began working together to say, okay, we need a new system one that replaces this because this one isn’t working for us. So when you read the Chinese readouts of the visit with Putin, for example, which we do, Xi Jinping is going on about how we shall not rewrite the history of World War II or redefine who the winners were.

What does that mean? That means exactly what I’m talking about right now, which is you can’t just sanction us. We won World War II alongside you if you’d like to fight it again. When you read Putin’s speech that he just gave at, um, St. Petersburg International Economic Forum or whatever it’s called, he’s of course very verbose. It’s like you print it out and it’s 40 pages long. From the Kremlin’s website, but they trace everything back to World War II. The war in Ukraine is framed as a refighting of World War II.

The rise of Japan and the military rearming of Japan and Germany are viewed by Russia and China through the lens of World War II. And the sanctioning of Russia and China is viewed through the violation of the post-World War II architecture that was meant to keep the peace. And so in our view, what comes out of all of this is a world where gold reasserts itself as a neutral reserve asset.

China and Russia are clearly preparing for that. What has postponed that has been sort of the omnipower of the US military enforcing US dollar hegemony. But can that go on given the current fiscal situation in the US, given what’s happened in Iran, given what’s going on in Ukraine? We don’t think so. So once this war is over and things settle down, we— there’s a reason I own as much gold as I do, and hopefully, you know, we’ll be rewarded.

Monetary Metals

What about silver? Obviously, there’s this kind of consumable oil, energy, materials market where commodities have seen falling prices generally. And then you’ve seen the kind of monetary metals, which are gold and silver, which have had incredible price runs in 2025 and 2026. Or as you mentioned, you know, you’ve seen the purchasing power, the value of these fiat currencies declining or depreciating. Where do you see the kind of breakdown for the future of silver?

Obviously, it has that monetary metal component like gold. Gold, but it also has that industrial component as well. Do you think that, you know, silver is going to have more of a sway in one direction in the future, rather monetary or industrial? Or do you think that it’s basically going to kind of plod along halfway between gold and something like copper?

Doomberg

I mean, I always annoy the silver bugs when I say this, but silver is not a monetary metal. It is an industrial metal. It is driven by supply-demand in fields like the solar industry. It is not as inert as gold. Its stock-to-flow ratio is wrong, and it has major industrial uses for which supply-demand dynamics then impact price. Same thing with platinum and palladium. And so the thing we’re writing about China and solar and renewables and why, you know, this is probably going to come as a surprise to you, Ben, but are you aware that China is installing far less solar in ’26 than it did in ’25?

Probably not, because all you see in the Western legacy media are articles falling over themselves, heaping praise on China’s climate leadership, which is ironic given how much coal plays such an important role in its energy envelope. There’s a collapse in installations in in solar in China, which we think is net bearish for silver and one of the reasons why we would avoid it. But silver’s just, it has an echo of Monetary Metals, sort of a bit of a scent to it, but it’s not a monetary metal.

And I think no central bank is stockpiling it, for example. And so it’s more copper than gold. And so if you’ve done a bottom-up analysis of the supply-demand dynamics of silver on a multi-year basis and you feel comfortable that the demand for silver will exceed the supply coming from mines, which admittedly are byproducts and all of that other stuff, I’ve seen all the arguments. I’m aware of them. Then great, go buy silver, but don’t buy it because you think it’s a monetary metal.

Rapid Fire: $40 or $140 oil? Nuclear? AI bubble?

Monetary Metals

Doomberg, we always love having you on for comments exactly like that. I want to take us into a rapid-fire round, so I’ll ask you questions from all over the map. You can answer as short as you want or as long as you want. So let’s start our rapid-fire round with oil. What do you think is more likely for us to see within the next year? Oil at $40 per barrel or oil at $140 per barrel?

Doomberg

In the next year, I would say $140 if only because I believe the prospect of escalation in the Middle East is higher than a true glut materializing in that short period of time.

Monetary Metals

Next question, still on energy in this rapid-fire round, is about nuclear energy. Obviously a lot of the AI data centers have said, oh, we’re going to open a nuclear power plant right next to our data center so we don’t touch the town’s energy infrastructure. How important do you think this nuclear question is going forward? In terms of the energy abundance portfolio we’ve been discussing?

Doomberg

I would say natural gas is a far more important fuel than uranium, just given the speed which new natural gas facilities could be stood up, as proven by Elon Musk’s wildly illegal natural gas plant that he put into Nashville that is now, you know, Anthropic’s key compute center. So yeah, we would say we’re bullish nuclear, we’re bullish uranium, but not quite as bullish as the AI narrative would have most people believe.

Monetary Metals

Now let’s pivot to that AI narrative. Is this AI narrative a boom where we’re gonna see, hey, these AI data centers, they’re real, they’re gonna produce economic value, and therefore this whole energy, materials, commodity supply chain is gonna come along for the ride? Or do you see this AI as more of a bust potentially where it turns out the economic value really isn’t there for what we thought AI was gonna deliver? And therefore all the downstream effects from the data centers to the miners, to the oil, to the energy market is also gonna suffer.

Doomberg

Can I say both? Because I think both are true. Look, our own personal interaction with AI in our private investing side of things, it is a revolutionary technology. It is mind-blowing. It is probing the very definition of what it means to be human. It will transform the economy. All of those things are true, and we’re in the greatest stock bubble of all time.

One wonders whether this SpaceX IPO might be the catalyst that pops it. I wouldn’t want to try to catch the falling knives. 10 years from now, the AI revolution will be real, will manifest. It will alter humanity, alter the economy in ways that are even impossible for us to contemplate today. And I wouldn’t buy the stock market with a 10-foot pole from here at these levels.

Monetary Metals

Now I want to ask about our friends, the Europeans. Obviously, we’ve been talking about the Middle East. We’ve been talking about the US. We’ve been talking about China. Where does Europe sit in all of this? It feels like they’re a little bit off to the side. They’re not that dominant player that they once were. Is this kind of a bottom for the European markets and for the European economies, or is this a knife-catching scenario?

Doomberg

I wouldn’t get long Europe until all of Starmer, Macron, Mertz, and von der Leyen are out of work. The current slate of European leaders is just so out of step with physics and geopolitics and reality that it is mind-boggling. We’ve often pointed out before the Strait of Hormuz closure the European Union, that the 27 member states of the EU consume 38 exajoules of hydrocarbons and only produce 5. That’s not a great spot to be in. Nothing on the board says anything’s going to change until the current leadership are wiped away. They will be wiped away. I watched the E3 countries with Zelensky earlier this week. You know, Starmer’s approval rating is what, a baker’s dozen?

Mertz is under 20. Macron’s, you know, politically dead man walking. Like, what are we doing? Like their collective of approval ratings added together don’t sum more than 50%. That which can’t go on forever usually doesn’t. I see, you know, Great Britain is erupting again in protest over a pretty ugly event that has occurred. I’m choosing my words carefully. The suppression of populism can only go on for so long. We’ve said for years that on the path from abundance to starvation is riot, first political and then physical.

Let’s hope we don’t get to physical. Getting dangerously close to physical in Great Britain, similarly in France. And so let’s see, they are stuck in a do loop of failed policies with a slate of know-nothing leaders who are resistant to leave. And so until the leadership is rolled over, one wonders how things get better.

Europe is uninvestable & the “Ozempic moment” for energy

Monetary Metals

I want to ask you now about the energy market. Is there an Ozempic moment for the energy market where all of a sudden there’s been this issue that we haven’t been able to fix? Maybe it’s nuclear energy, maybe it’s fusion or fission. And similarly to Ozempic, you know, we’ve had this obesity issue and now all of a sudden with these new GLP-1 drugs, people are losing weight.

This could have ramifications on food, on health care, on so many facets of the American lifestyle. Is there a similar moment that we’re waiting for in the energy markets, or is it actually more of a kind of slow and boring story? Well, as long as things keep going up into the right, this energy market will be an abundance energy market rather than a scarcity market.

Doomberg

Market? I hope there isn’t an analogy to the weight loss drugs because I would stay far away from those. You are fundamentally altering the human body in ways that our collective creator certainly did not intend. I would say the root cause of the obesity issue is the quality of the food supply in the Western world, and I would much prefer to see a solution that tackled that. Not that that’s anything we’ve written about or will ever write about.

To your question on energy, I just think that if I see a 60-year trend, I’m just going to bet on it. There isn’t really a need for a huge step change in the case of deflationary technological development in the energy sector. It’s there, it’s real, it’s happening. The speed with which Exxon brought Guyana online, which was the heart of the presentation we went over last month, just shows you the power of these true technology companies, you know, in our space.

And again, if you ask me like, what is the potential magic bullet energy technologies or developments out there, I would not say it’s fusion. Fusion, it’s a fake technology that solves problems that don’t exist, which is something we can get into if purchased it at some point.

But I would look at things like natural hydrogen. I think there’s an enormous amount of hydrogen underground that can be drilled for. That would be a real game changer. I think we’re on the cusp of some game-changing stuff in geothermal. We’ve made some private investments in that regard. The drilling technology that enabled the shale revolution is going to enable geothermal in a way that probably few people are prepared for.

Monetary Metals

But again, all these are additive and ultimately, you know, the up and to the right curve of primary energy consumption will Now I want to ask you about the Doomberg mental model because a lot of energy analysts are way off and they say things and never turn back and say, actually, we got that wrong. Here’s why we updated. So what’s the Doomberg mental model that you guys use to analyze the energy markets that’s different than other energy analysts?

Doomberg

Yeah, so I should probably define that term. You know, we pride ourselves on lateral thinking. To be a lateral thinker, you have to have no emotional attachment to the correctness of your axiom. It just has to work. Book. It just has to explain things. Once it stops explaining things, you have to discard it. And our current operating mental model among many is that oil and gas are best modeled as being in infinite supply, and it’s just a matter of bringing them to the surface. In other words, peak cheap oil is a myth. We’re swimming in light hydrocarbons.

So if you model US natural gas supplies as infinite, then the midstream buildout and everything else that we’re seeing make a lot more sense. And we’re not running out anytime soon. So if your mindset is one of scarcity price spikes that flow from that, we just think that that’s a mistake. And the war in Iran in a way has kind of proven that. There’s just so much of this stuff and there had been more than the market was letting on for much longer because the Chinese were soaking up all of this extra supply to stick it into inventory.

And so that is our operating mental model for hydrocarbons. We have many operating mental models. I’ll give you another one that we’re working on for this piece on China and solar right now, which is that a grid can’t withstand intermittent renewables once intermittency exceeds dispatchability. In other words, the sum of natural gas and hydropower tells you when things begin to break because coal and nuclear aren’t that dispatchable.

And that’s what we’re seeing in China today that we predicted last year that’s coming through now. Back to this decrease in solar installations in China that I referred to earlier, that’s one mental model. By the way, in the piece we’re publishing, we’re going to go into how that model might fail and when we change our mind because we have no emotional attachment to the correctness of it. Just, just as long as it’s working, we’re going to run with it.

And so we’ve seen no evidence that the hydrocarbons are in short supply geologically. All we see are evidence that is that politics and war and, and so on get in the way of the extraction of, of this stuff. And so for the length of anybody’s listening lifetime, there’s going to be more than enough oil and gas underground.

The Doomberg Mental Model: Oil is infinite, gold is the future

Monetary Metals

And I want to ask you now about the mental model for gold listeners. Now, is there a useful mental model you guys use for the gold market? Obviously the stock-to-flow ratio is incredibly important for gold that we discussed compared to other asset classes. Is there a certain mental model or, or kind of alpha in the Doomberg mental model when it comes to gold versus some other assets?

Doomberg

So in our view, the sort of proxy for gold, and as I said, go back and actually plot it, the number of US sanctions over time against the gold price would be an interesting thing. As I’m sitting here pondering, like some things you just feel intuitively.

Monetary Metals

Yeah.

Doomberg

What is a sanction? A sanction is increasing the friction of utilizing the dollar slash US treasuries as neutral reserve assets. So if you are prohibiting the functioning of a store of value of a US Treasury by deciding who gets to own it and who doesn’t, then you are forcing people into an alternative. And that alternative, in this case, the only alternative, the one that everyone believes has this multi-thousand-year history, is gold. And so I’m probably going to do that now.

Like, I’m sure there’s somebody who’s just literally counting the number of sanctions the US Department of the Treasury publishes over time, and I’d be very curious to see see in broad strokes how that does against the price of oil, because I do think this phase shift that we saw in 2014 is again the genesis of this war that we’re seeing.

And, and I think one of the mental models that is tied to gold because of this whole setup I’ve just laid out for you is that if you’ve sort of viewed the war in Iran and the war in Ukraine as a holistic war of attrition by Russia and China and their proxies and friends against the US military’s inventory of weapons, once that inventory is exhausted, then you could roll out your gold back BRICS currency is the wrong word, but what’s really needed is not sort of a unit of exchange.

It’s a store of value. If I’m going to trade with China and I end up with a bunch of currency I don’t want, I could go ahead and trade into gold with zero friction, and then gold becomes that neutral reserve asset that nobody minds if it goes up in value against all the other currencies, which is kind of what’s happened since 2014. So that’s our sort of mental model for gold. The more, you know, once you uncork the sanctions genie, it’s really hard to put it back in the bottle.

It’s kind of like deficit spending with the printer press. And so the more the US Department of the Treasury sanctions companies, that’s why we thought this sanctioning of Henli in China was such a watershed moment. And China finally saying, we’re going to institute our sanctions blocking law. That is sort of the beginning of the end. If China can stare down Scott Bessant on sanctions, then, you know, the rest of the world can begin to revolt against this system too.

Monetary Metals

And do you see that going forward that there will be this, you know, neutral reserve asset in gold where people say, say, hey, maybe you owe us rupee, or you owe us ruble, or you owe us yuan. We obviously don’t really want yuan in our country or rupee in our country, but we’re happy to do that kind of net trade settlement in gold.

Do you think that’s something we’re going to see more and more in the future as countries say, well, this friction that’s being created, whether through sanctions or whether through other kind of dollar weaponization, do you think that’s going to push people to this kind of gold trade settlement? Or on the other side, do you think that this dollar stablecoin distribution, where now these private companies are distributing US dollar access through these cryptocurrencies or stablecoins, do you think that that actually pushes the dollar hegemony even further than it has been before?

Doomberg

So, you know, I think both are going on at the same time, but I saw Scott Bessant on CNBC bragging about all the crypto wallets he had just confiscated. What are we doing? Like, have we not learned? Right? And so once you open the sanctions genie and you sort of get drunk on that power that I could just by dictate say this person is no longer— they’re an unperson in the economy. It’s hard to go back.

And so if stablecoins are then suddenly viewed as just another asset the Department of the Treasury can confiscate, maybe you do want to get that account on the Chinese payment rails and store your value there because China thus far has not performed in the same way at all, especially if you’re in the Global South.

Now look, if you are you or me or somebody in Europe who has, you know, lives in the dollar fiat system and has children in college and bank accounts and, you know, you’re not going to partake in such liberties. But if you’re in the Global South, if you’re in China, if you’re in Russia, if you’re in Iran, if you’re in India, if you’re in Brazil and you’re looking around saying, do I want to store my stuff in a stablecoin? Or do I want to get on, you know, Alipay? Probably going to put Alipay on your phone.

Deglobalization, tariffs, and Trump’s closing window

Monetary Metals

Now I want to ask about that kind of fracturing of this global trust where we had a global economy where we said, hey, whoever can do something the cheapest, whether it’s in India or China or Russia or wherever, let’s do it because that’s this global infrastructure, this global supply chain. It will create efficiencies. Obviously, Trump and this regime have said, hey, we want to think more about America first. We want to have this kind kind of deglobalization trend.

There’s tariffs, there’s trade wars, supply chain disruptions. Do you think that we’re kind of hitting that new world order where people say, hey, we’re in a multipolar world and the order that we used to have with efficiencies and global supply chains is over? Do you think we’ve basically hit a peak in the level of global efficiency from companies saying, hey, we’ll work with you no matter what country you’re in, and from here on in we’re going to see kind of a fracturing of this global order?

Doomberg

The victim of all of this has been the US manufacturing base.

And in other words, in order for US Treasuries to serve as neutral reserve assets for the settlement of imbalances in international trade, there had to be a lot of them, which meant not only was it okay for the US to run deficits, but it was also sort of necessary. And the grinding away of the US industrial sort of complex serving the military after World War II, which looks so dominant, was so dominant, was as dominant as any military-industrial complex has ever been.

That has been ground down since the closing of the gold window. And Trump correctly diagnosed the problem and campaigned on fixing it, which again is why the war in Iran is so counter to all of that. The way to have fixed it was to radically lower the value of the dollar. In other words, for gold to skyrocket, to turtle into the Western Hemisphere, fix up the home base, get manufacturing back. And he was doing that in the first You’re, you know, going to all of the Arab sovereign wealth funds, and they were pledging trillions of dollars to invest in the US.

And now all of that, of course, is up in smoke, literally, because like, wait a minute, you know, when was the last time you heard about Trump’s peace port, right? I mean, come on. And so here we are, that momentum has stalled. The détente that Iran has been able to achieve has laid bare the weakness of the US military compared to perceptions, not in absolute terms, compared to perceptions. And yet the industrial base of the US has not yet been rebuilt. And so we’re kind of stuck in the worst of all worlds.

And then the left-leaning response to Trump that’s coming is going to undo a lot of that too. I mean, one of the great shames of all of this is there was this generational opportunity to fix things like permitting and pipeline construction and all the stuff that’s necessary for the US to make full use of its energy advantages. And so I do think Trump in the back of his mind knows this, needs to get this war in Iran wrapped up, would like to do it before the midterms. But here we are.

Monetary Metals

And I want to ask you now on that kind of political front, do you think this potentially coming stalemate in U.S. politics means that whatever we’ve basically gotten out of Trump— yes, maybe on the margin there’ll be some additional changes, but basically what we’ve seen from the Trump administration so far is what we’re going to get in terms of policy. Or do you think there are actually some more final pushes, whether it’s the Clarity Act, whether it’s some other pieces of legislation? Do you think that basically what we’ve seen is what we’re going to get out of the Trump administration? Or that there’s more surprises coming?

Doomberg

I mean, much depends on November, of course. But, you know, one of our operating mental models was that, you know, in a blind vote in Congress, Trump would have been impeached and removed. I mean, that there’s very little support for Trump in the U.S. Senate. I—there are no Republicans and Democrats in our mind. They’re all the uni-party team members that just happen to wear different jerseys. And we’re seeing that now, you know, the recoiling at this J6 fund that Trump had set up, you know, his settlement with the IRS.

The fact that, again, under the radar, and we’re not a political newsletter, but Trump’s endorsement of Attorney a sitting longtime Republican senator did not go over well with the Republican caucus. You know, this is not, not how things are meant to be done. And I think we’re going to see now going forward far less support for the president’s agenda. You already have all of these judges all over the country ruling against Trump, I think dubiously, but still happening, throwing wrenches into the gears. And so even, executive actions are stunted by the judicial branch. You have very little support in the Senate for the president.

If the Republicans suffer defeats in the midterms and at least one of the houses flips, then all of a sudden you’re looking at investigation after investigation and committee hearings and testimonials and all that other stuff. Impeachments, even if the House flips. And so you’re going to see a distracted president. And then already after the midterms, everyone will be gearing up for 2028.

So you’ll see Newsom against Harris and you’ll see JD and Rubio sort of navigating with DeSantis in the background. And so it gets pretty messy. And one of the big challenges, we wrote a piece called Whiplash shortly after Trump became president again for the second time, which is the capital planning cycle of every industry is longer than the political cycle for the US by a wide margin. And this type of whiplash is not very good for the president’s admirable long-term objectives in the energy space.

Look, I mean, we cheered loudly the appointment of Chris Wright as Secretary of Energy, and we were strongly supportive of the president’s energy policies, whatever flaws of the man or his other policies that you might object to. I think on energy, he was stone cold dead right, and he’s gotten a lot done, but not enough, and the window’s closing.

What would prove Doomberg wrong?

Monetary Metals

All right, last rapid-fire question here. We’ve talked about this energy abundance idea. What would you have to see in terms of maybe a headline or something as in the facts base to make Doomberg go, you know what, I was completely wrong about this future of energy that I kind of foresaw or foretold? What would have to be in the fact set for you to say, yep, you know what, we got that one wrong?

Doomberg

The mental model of infinite hydrocarbons? Is that what you’re asking? I mean, I don’t know. I mean, that is so foundational to our analysis that I think we’d have to hang up the shingle at that point. There’s just so much of it and so much evidence for it that it’s almost like a law of physics at this point. I can’t conceive of a world where that foundational assumption is wrong. It’s just, again, decades of experience, decades of market observation. You’re basically making a short bet on human ingenuity, and I would just never do That’s why we love having you on the podcast.

Monetary Metals

All right, last question for me. What’s a question I should be asking all future guests of the Gold Exchange podcast?

Doomberg

Why aren’t you a pro subscriber to Doomberg? And if you aren’t, what is your plan to fix that situation by the end of the day?

Monetary Metals

All right, listeners, if you’re not a pro subscriber, you absolutely have to. Doomberg, where can people find more you and more of your work?

Doomberg

Yeah, you can find us at Doomberg doomberg.com. Everything is there. I should say our annual subscribers, regular subscribers, get roughly 90 articles a year, and then our pro subscribers get those articles and then our fixed presentations, which we put out once a month, deep dives. We’re doing a deep dive this month on Argentina, vaca muerta. Next month will be China through the lens of energy. That’s for our pro tier. Ben, it’s always great to come on your show. Uh, it’s always a pleasure. Enjoy our conversations. Really enjoyed this one and looking forward to the next one as well.

Monetary Metals

Doomberg, thanks so much. And if you guys aren’t subscribed by the end of the day, we’ll have to hunt you down in the comments. Thanks so much.

Follow Monetary Metals on X: @Monetary_Metals

Subscribe to Doomberg’s newsletter: Doomberg.com