George Gammon on the hidden risks of dollar strength

Many investors worry about a weakening U.S. dollar, but are they watching the wrong risk?

In this conversation, George Gammon argues that persistent dollar strength could place growing pressure on foreign economies, disrupt global trade, and create unintended consequences for the United States.

By exploring the relationship between credit creation, global liquidity, gold, interest rates, and financial crises, he challenges several widely held assumptions about how the monetary system works.

This interview offers a thought-provoking framework for understanding today’s macroeconomic landscape—and what investors should be watching in the months ahead.

Watch the episode now.

Transcript

Intro & high level macro view

Monetary Metals

Hello, everyone. I’m Dixon Buchanan, Monetary Metals. And I am doing my best to fill in for our regular host, Benjamin Nadelstein, who couldn’t be with us. But I’m here today with macroeconomic expert George Gammon. And George, I’d love to just start with what is your high-level macro view over the next 6 to 12 months?

George Gammon

I think what everyone is missing right now is the dollar, believe it or not, because the narrative is the dollar is crashing. And the narrative is that foreigners are dumping Treasuries because they want to kind of divorce themselves from the United States. And I think the bears are a little surprised the DXY is still trading at roughly 99. And the bulls are kind of—everyone’s pointing at them saying, well, I thought the dollar was going to 110. And again, I’m just using the DXY as a proxy. Sure.

But I think once you scratch beneath the surface, it tells a much, much different story.

So as an example, most people know the BOJ has been trying to defend the yen at 160 to the dollar. And so they’ve been doing this for like call it 6 months, 9 months. And the DXY, we have to remember, is 13 or 14% yen. So we have to realize that that 160 number is not a market number at all. So you sit there and ask yourself, okay, what would the market number be? Nobody knows, but it sure as hell wouldn’t be 160. Say it would be 200 or 210 or something like that.

So then you’ve got to ask yourself, okay, where’s the DXY if yen is at 200? You know, okay, it’s not at 99. I don’t know the exact, you know, math behind it, but is it 105, 110? And if the DXY is at 110 versus 99, it’s a completely different narrative, like totally different narrative. Now, in connecting the dots here, I think most people have read in the news a lot of the central banks such as Turkey are not only selling gold, but they’re selling their US Treasuries.

In fact, it was dramatic with the Turkish central bank from the standpoint of like a month ago or 2 months ago, they had $15 billion in Treasuries and it’s all the way down to almost zero. So, you know, what are they having to do right there?

The Dollar Wrecking Ball: Asian currencies are getting crushed

George Gammon

Well, they’ve got problems because they’ve got to import all this oil and the oil price is going up and then their currency is going down. So, you got to somehow defend that currency. So, gas prices don’t go up, you get social unrest.

We know how this plays out. So, they’ve got to sell those treasuries to get the dollars they need, which is a similar situation to Japan in the sense that they’re trying to defend that currency to make sure that the local energy prices don’t go through the roof and they get that same type of social unrest.

But these are—stories that you don’t really hear about. If you do hear about them in the mainstream media, the mainstream media isn’t connecting those dots. Another one that directly applies to this is the Indian rupee. So if you look at a 5-year chart of the Indian rupee, it’s just—it’s almost like up in a straight line. And what this is doing is telling you how many rupees you need for $1.

So as this chart goes up, that means the dollar is appreciating in value relative to that local currency, right? So they’re just getting absolutely crushed. And then India is another country that imports a lot of energy. And what we have to realize is energy, there’s very inelastic demand. It’s not like going out to the movies or something like that. Like, if you got to put gas in your car, you got to put gas in your car.

Monetary Metals

You can’t go without energy.

George Gammon

That’s right. You got to think about it this way. Let’s use Japan. We look at Toyota. That’s kind of like a proxy for Japanese exports and manufacturing. So if Toyota is selling $100 worth of Toyotas to the United States, they’re going to get $100 coming into their country.

And if their demand for oil is $100, that works well because then they have to have $100 going out to get that oil that needs to come into the country. The big problem here, of course, is not just if the price of oil goes up because then they need more dollars and therefore they have to use more yen or sell more treasuries, but also if the value of their currency relative to the dollar goes down, right?

So if they have $100 in oil and the price of oil doesn’t change, but their currency goes down in value relative to the dollar, they still have to have more of their local currency to get the same amount of dollars that they need to buy the same amount of oil. Then what exacerbates this is when you have tariffs, when you have—and you can say they’re right or wrong, whatever—but the bottom line is it slows down the, let’s say, circulation of goods and services globally.

It slows down the global economy. Well, what that means is instead of $100 coming in by selling Toyotas to the United States, now you’ve only got $50, but you still got the same $100 going out. So where do you get the extra $50? You either have to do what the Turkish Central Bank is doing, sell assets, Right. But what happens when you run out of assets? Then the only other asset you have is your local currency.

Monetary Metals

I see. So it’s further depreciation.

George Gammon

Absolutely. Because then you just take your own currency that increases the supply on the global market of the Japanese yen, but then it increases the demand and then you go into like this doom loop type of thing. And so it’s just not on anyone’s radar because the DXY is just pegged like at 98, 99 because you have this market manipulation for one of the reasons because you have this market manipulation from the BOJ and most Americans really don’t focus on Asian currencies.

And why I mentioned the Indian rupee, it’s not just the Indian rupee, it’s the Japanese yen. Like we said, it’s the Korean won, it’s the Philippine peso. I mean, it’s almost every single currency in that Asian bloc is just taking it on the chin from the dollar. And if it continues to get worse and worse and worse, it could completely blow up their economy. You say, well, how? You just got to put it in terms of what we can understand, right? So lately, the price of gas in the United States, let’s say nationally, has gone from $3 to, let’s just say, $4.50, something like that.

Monetary Metals

That’s what I’m paying.

George Gammon

Yeah. And everyone’s like freaking out about it, right? The Republicans are losing the midterms. Everyone’s freaked out about that. And look at the consumer sentiment numbers. They’re all in the absolute tank. And the main reason is because oil has just gone up $1.50. Let’s say the oil or gas was denominated in another currency and then the dollar is going down against that currency.

Well, that means that gas wouldn’t go to $4.50., it would go to $8, $10. Right. So think about gas going from $3 to $10 instead of $4.50. What would that do to the US economy? You can be the biggest bull on the planet Earth and you’d have to admit that if gas goes to $10, you know, we’re likely gonna have a big, big, big economic problem, which is gonna lead to some severe social unrest. And then you gotta say for manufacturing, you know, your input costs are now $10 as far as energy, just using that as a proxy.

Monetary Metals

Sure, sure, sure.

George Gammon

As instead of $4.50, how can you make your widgets? And then how can you export? Then your exports go down. And you see how this can really start to grind an economy to almost a complete halt.

Monetary Metals

Now, is that a risk primarily for foreign nations? Like, is the US somewhat insulated from that effect?

George Gammon

Absolutely.

Monetary Metals

Okay.

George Gammon

Absolutely.

Monetary Metals

So talk a little more about that. Like, is it—

George Gammon

Yeah, so they have to worry about two things. They have to worry about the price of oil, but then they also have to worry about their currency relative to the dollar. We only have to worry about the price of oil, right? Because all of our expenses are actually denominated in dollars. That’s a very, very good point. But that kind of goes into what I’m talking about. So most people, when you see the narrative, especially if you go to the, you know, the gold conferences or something like that, the narrative is that the dollar is going to crash.

Now, the first thing you have to do there is you have to differentiate between the dollar crashing against goods and services, because that’s one thing, and then the dollar crashing against other currencies. Those are completely separate topics, and most people conflate the two, right? And they assume that if one thing’s happening, the other thing’s happening, and quite often it’s the complete—

Monetary Metals

sure—

George Gammon

opposite.

Monetary Metals

The former technically has been happening for many, many years. It’s kind of in a freefall. Yeah, just a different velocity. Yeah, but the latter is much more variable. You get ups and downs. It looks like, you know, pull up any two currency pairs and you’re gonna see a lot of different movement.

George Gammon

Yeah, so as an example, in 2000, the DXY was maybe 120. I mean, it’s high, like really high. But then you fast forward to 2011 and it’s at 70, right? And then you fast forward today, you know, it’s almost back up to 100. Now in that time frame, what happened to the dollar relative to goods and services in the United States? And we all know it just goes straight down, right? It just goes straight down. So that’s really a given.

But what can happen is the dollar can appreciate in the United States substantially not necessarily against goods and services, but against assets. So what did we see during the GFC? You know, we saw the S&P 500, let’s say, go down to whatever, 700 from 1,500. So that means that it’s absolutely crashing. But that means that another way to say that, you buy more S&P, is the dollar is appreciating massively against the S&P 500, or it appreciated massively from 2006 to 2012 in terms of housing. Sure. Right.

Monetary Metals

Yeah.

George Gammon

So against assets, the dollar can really appreciate in the United States. But again, to your point, against goods and services, the probability of the dollar increasing in value is almost zero.

Monetary Metals

It doesn’t have a good track record.

George Gammon

No, no, no, it doesn’t have a good track record.

Monetary Metals

I want to—I want to bring gold into this, right? Yeah. And I’m just curious to hear your take. Obviously, we’re a gold company and we’re in the gold business. The statement that gold is the best measurement of the dollar. I know. So, so what’s—yeah, so I see some of your reaction to that. So what’s your chief argument against that?

George Gammon

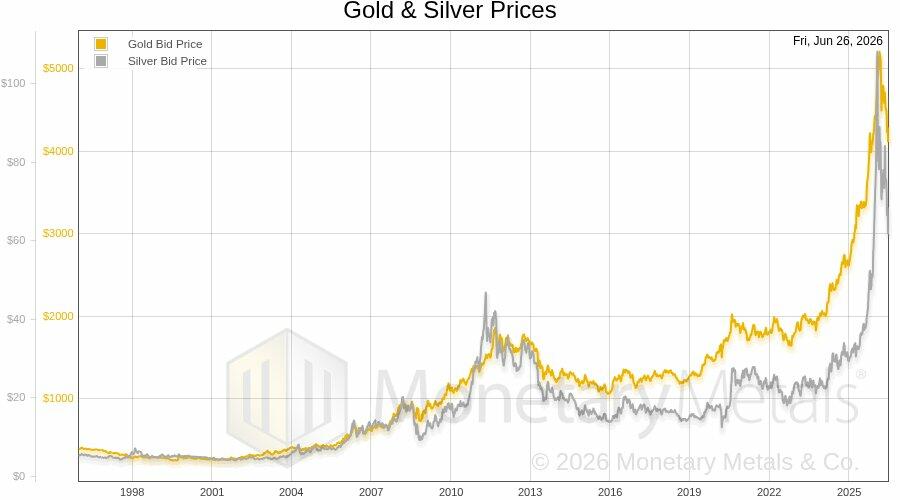

Look at a chart. That’s all you got to do. Just look at a chart of the gold price, what I’m saying, and look at a chart of anything else that you think impacts gold. So look at the chart of the DXY, look at a chart of the CPI, look at a chart of the US debt, look at a chart of the debt to GDP, look at a chart of the deficits, look at a chart of anything you want relative to gold. And at times you might see a correlation like in the 1970s, right? So CPI up, gold up.

But then at other times you’re going to see CPI up or CPI down. Like as an example, you know, did inflation spike massively from 2000 to 2011? Not really. In fact, it went down. You had disinflation. You had the price of gold just go straight up, almost with the exception of the GFC.

Gold is not an inflation hedge (here’s what it actually is)

George Gammon

There are times when you can find that correlation, but if you really zoom out, you see that it’s at best a coin toss. So the only thing that I’ve been able to determine is that over long periods of time, gold absolutely unequivocally holds its value.

There is no disputing that. But you could take like 5-year segments to where it does the complete opposite of what you would think. I mean, look at right now what’s happening, right? Gold is almost inversely correlated to oil.

So you would think that if oil is going up, oh my gosh, inflation, you know, gold’s got to be ripping higher. When, as we’ve seen, when the price of oil goes up because of a Trump tweet or something like that, usually a lot of times the price of oil will really go down. So the only thing that I’ve been able to determine at all all really drives like a short-term move in gold is just really counterparty risk.

Monetary Metals

So in periods where counterparty risk is high, yeah, there’s a bias to hold metal.

George Gammon

And then, yeah, that’s what I’ve seen. But just the way it pans out though is just over long periods of time, it’s just you can still buy—what is it, like a suit for an ounce of gold? And you could do the same thing back in 1900.

Monetary Metals

And it’s true though, these days you’d be buying a really good suit at these prices.

George Gammon

Yeah, that’s true. That’s true. But it just kind of works its way out. I would be willing to bet that in 100 years you’ll probably still be able to buy a suit for an ounce of gold. That’s really the genius. That’s why I think everyone should have gold in their portfolio. It’s not to get rich, but it’s to stay rich.

Monetary Metals

Keep what you own. Yeah.

George Gammon

And I think that going back to the dollar, most people look at the fall of an empire or a civilization and they associate that with the demise of the currency. So it’s like they almost assume that if an empire is falling, that one of the main contributors to the fall of that empire is the decrease in the value of the currency. Sure, the currency crashes or whatever. I think with the United States, if you believe that the United States is in decline—I still think the US is the greatest country on earth, but it’s in decline. Hopefully we can turn that around.

Monetary Metals

Sure.

George Gammon

Yeah, you know, but, but I think it is showing signs of of, let’s say, weakness. But I think that in, in this scenario, assuming that the United States continues in that direction, that we could actually see the opposite. And what I mean by that is the decline of an empire—actually, the catalyst for that could be the currency going up and not down. So let’s go back to what we were talking about.

Monetary Metals

Tough thing to like kind of get your mind around, so I’m wondering if you can like make that super clear for us. Sure. I think everyone would almost default to the opposite. So yeah, so what do you mean by that?

George Gammon

So So we go back to India, we go back to Japan, and we talked about how the dollar going up can absolutely decimate the economy.

Monetary Metals

Sure.

George Gammon

Can decimate the economy.

Monetary Metals

But that’s the foreign economy, not necessarily the, call it, US economy.

George Gammon

Correct.

Monetary Metals

Okay.

George Gammon

Okay. So one story I always like to tell is go way, way, way, way, way back in history to around 1100, 1200 BC.

Monetary Metals

Okay.

George Gammon

Okay.

Monetary Metals

All right.

George Gammon

So at the time, the big superpower back then was Egypt. Okay, and they had one of the pharaohs, you know, his name was Ramses III. Okay, and he was known for his, you know, military strategy and whatnot. And during this period, they have this infamous group of people who were effectively pirates, and they called them the Sea Peoples. Okay, right.

And some people back in those times, they actually thought they were aliens, and there was all these stories about them, right? That’s why I say they’re infamous. And back then, you know, the whole world was basically the Mediterranean. Right, or the known world, right, right. And so the Sea Peoples, they started at like the top and they just went down the Mediterranean coastline and just wrecked shop on like every single major city.

Monetary Metals

Okay.

George Gammon

They would just park their boats out there and then the city would try to send their little navy out there and they just get decimated. And they’d come in and they just rampage the whole city, steal all the gold, and, you know, do whatever else they’re doing. And then they just move on to the next city and seek and destroy. They had this reputation like they’re like superhuman.

So what happened is as they kept going down, their legend became more and more and more and more powerful, right? Like Tiger Woods, to the point where you see him and you might as well just give up because there’s no way you’re going to psychologically beat him, right? Right. So anyway, but they knew that they’re coming all the way down and they’re headed for Egypt.

Monetary Metals

Okay.

George Gammon

So the Egyptian people, they’re like freaking out, like, oh, what are we going to do? And everyone’s scared. And they knew that they’re coming for them. And the Ramses guys is like, okay, I got it. I got an idea. So he didn’t want to fight them out in the waters So what he wanted to do is try to draw them into the Nile, the Nile River.

So he drew them into the Nile River where he consolidated their navy, and then he had all of his archers hide in like the cattails and whatnot, you know, where they found Moses. Yeah, yeah. And they had all the archers hang out there, and then when the Sea Peoples came in, the archers ambushed them and just—and like took them out, and he won. Ramses did.

Monetary Metals

So that is a fascinating story. How does that tie to the dollar and what we were talking about earlier?

George Gammon

I’m glad you asked. So what happened is everyone in Egypt was excited and they’re partying and Ramses is like, you know, he’s a big shot and he’s telling everyone how great he is. But what happens 6 months later or a year later or something like that?

The dollar sea peoples: how a strong dollar breaks empires

George Gammon

Their whole economy collapses, their whole empire collapses. And a lot of people blame the collapse of the entire Bronze Age on the Sea Peoples. But so what happened, right?

Monetary Metals

Yeah, what happened?

George Gammon

Because they woke up after the hangover, you know, if they were partying and celebrating and like, wait a minute, who are we going to sell bronze to? Oh shit, we don’t have any trading partners.

Monetary Metals

So they destroyed their counterparty.

George Gammon

That’s right. Who are we going to get silk from? Who are we going to get wheat from? Who are we going to get corn from? Who are we going to sell this to? Who are we going to do that to? There was no one left because the Sea Peoples took them out. So what happened is that ended up collapsing Egyptians’ economy, even though they won the battle with the Sea Peoples. So in this story, what is the Sea Peoples?

Monetary Metals

It would be the foreign nations, I would assume.

George Gammon

That would be the dollar.

Monetary Metals

The dollar. Okay. Make that connection for me.

George Gammon

So the dollar is the Sea Peoples.

Monetary Metals

Okay. It’s the one that’s destroying all the different counterparts. I see. I see. Okay.

George Gammon

Okay. To where if it destroys India—

Monetary Metals

So those markets just get—they get, like you said earlier, kind of ground under this relative dollar strength.

George Gammon

Due to the dollar going up. And again, I want to be clear, not the dollar going up against goods and services in the United—because a lot of people are going to be freaking out saying, are you kidding me?

Monetary Metals

You may have just saved yourself about 50 comments on the—on this video.

George Gammon

Yeah, but I get it, right? Because people are like, no, you know, my, my grocery bill has been going up. It’s not gonna—yeah, it’s right. You’re crazy. You’re crazy. No, I’m talking about the dollar versus other currencies. That’s the dollar wrecking ball, if you will.

That’s the dollar Sea Peoples where it’s just going to Turkey, taking them out, going to Japan, taking them out, going to India, taking them out. And if it goes to enough of these countries and it decimates their economy to the degree to which it can—it hasn’t done yet—the degree to which it can If you don’t believe me, just look at a chart of the Indian rupee. Right, right. And just think about how that works with energy that they have to have it.

You can see how this could lead to a doom loop where the dollar goes up so much, crushes their whole economy. Then the next thing, you know, we’re left standing. Who are we going to export to? Who are we going to get our stuff from? And that really is detrimental to the US economy. So that’s—it’s a little bit hyperbolic to say it’s, you know, the Roman Empire because the dollar goes straight up. I think it’s an interesting thought experiment. Sure. Because the narrative is so contrary to that.

Monetary Metals

Got it. I want to actually go back to Japan and the yen, relative strength of the yen. They have a new incoming prime minister.

George Gammon

Mm-hmm.

Monetary Metals

My understanding is that, you know, she’s pro-Japan.

George Gammon

Mm-hmm.

Monetary Metals

And that part of her agenda, part of her plan is to kind of rebuild the economic strength of Japan. And that could have a strengthening effect to that currency. Have you thought any about that? Like, what’s your take on that? Good luck. In what way?

George Gammon

Okay. So let’s just assume that you strengthen—I don’t know how you strengthen the manufacturing base of Japan because as a massive trade surplus as it is. So it’s not like it’s, you know, got a trade deficit or something. But let’s just assume that she—well, who’s she going to sell to? You have to go back to your overall macro view.

Now, if you believe, you know, with Trump in office and all these other things, that somehow the global economy is going to come back together again and really start to accelerate—and by the way, China’s in a depression. And let’s not forget about the second largest economy in the world is basically in a GFC right now. Jerome Powell, right?

But so if you think that the global economy somehow, with all the geopolitical risk, with all the protectionism, with the fourth turning, right, you know, with all these things going on, is going to somehow come back together and then start to really, really grow rapidly, you’re right. Then they, they’ve got a release valve, they’ve got an exit strategy. But without that happening, it’s not a matter of if the Xi peoples get them, it’s a matter of when.

So let me give you an example. Remember when I was talking about the dollar being at 120? In 2000, and then it goes down to 70 or so. What happened during that time frame? That was the emerging markets blowing up. That was China blowing up. That was the world economy just expanding at like breakneck speeds.

Well, if the global economy is expanding, you would expect the dollar to go down in value. Why is that? Because the Fed or the government, they don’t create dollars like people think they do. But really, the Fed’s balance sheet is almost irrelevant to to the amount of dollars that circulate in the global economy. Who creates them? It’s the banks, right? It’s the banks. So what they’re going to do is they’re going to create those dollars by lending them into existence. But the only way they’re going to lend more and more dollars is if the risk-reward makes sense.

Yeah, well, the only way the risk-reward makes sense is if that widget maker can make more widgets. And the only way they can make more widgets if the global economy is expanding. So not only would you have more dollars being created due to the emerging markets growing faster and faster, faster, because, oh, by the way, they need commodities, So they need dollars, so they need to borrow more.

But those dollars are going to circulate with more velocity, which effectively is creating more dollars. So if you have more dollars being created because of a global expansion and more demand for those dollars due to commodities and energy and whatnot, then you would actually expect the dollar to go down.

Whereas if you get a huge monetary shock and a blowup of the financial system that quite frankly has never been repaired—I’m talking about the GFC, right? Right, right, right. You would expect expect the global economy to start to sputter, right? It doesn’t collapse, but it ain’t running on all 8 cylinders. It’s running on 6 cylinders, right? So then you would expect the dollar to appreciate.

Monetary Metals

Sure.

George Gammon

Because the global banks aren’t going to be willing to create as many dollars because the risk goes up, the reward goes down. So the lending goes down. That means more loans being paid off than are being created. That means the supply of global dollars actually goes down. At the very least, the circulation of money and credit goes down, and that means dollar up because you have to have those dollars based on what we were talking about at the beginning of the video.

Japan’s new PM can’t fix this

Monetary Metals

So this is basically, to synthesize if I can, this is kind of the basic mechanics of credit expansion and credit contraction.

George Gammon

Yeah.

Monetary Metals

And in credit expansion, you would expect to see a lower relative strength of dollar. Credit contraction, it’s the opposite effect.

George Gammon

That’s correct.

Monetary Metals

Okay.

George Gammon

Because the dollars are effectively credit. That’s what they are because they’re lent into existence, right? People have to think about it this way. Set aside currency in circulation. Set aside the little green pieces of paper and a couple other things. I don’t want to get too esoteric, but we’ll just keep it super simple. So set aside currency in circulation, just cash, right? If you paid off all the dollar debt tomorrow, let’s say everyone pays off their car loan, their mortgage, all the banks pay off the interbank credit and, you know, all these things.

How many dollars do we have? Zero. Well, so if all the debt, dollar debt got paid off tomorrow, there would literally be $0, right? None, right? Zero. Once you understand that, you’re like, oh, now I get it. Yeah, now I get it. Now I understand why, you know, these dynamics in the monetary system actually exist. Because most people, they don’t think in terms of the banks creating dollars by lending them into existence. They think of the Fed printing dollars, you know, because they’re expanding their balance sheet. And in reality, that’s not the way it works, right?

Monetary Metals

I want to—like, we’ve kind of done a high-level flyover of a lot of different, you know, macro themes. I want to tie that to someone in the audience listening to this. They’re trying to allocate their own capital. Like, what’s the takeaway, or the 3 takeaways, for where we are right now for someone who’s looking to allocate capital the next 6-12 months, if not longer?

George Gammon

Well, the next 6-12 months, that’s a great question. I mean, I can tell you what I’m doing with my own portfolio. It might be a little—maybe people haven’t thought of. Number 1, you got to own gold. I mean, that’s just kind of a no-brainer, but it’s not really a speculation or an investment. It’s just more so like an insurance policy. That’s how I always treat gold, like 10% of the portfolio. It’s my kind of—

Monetary Metals

it’s kind of like a permanent allocation.

George Gammon

Okay. Yeah.

Monetary Metals

Okay.

George Gammon

That’s what I do.

Monetary Metals

Okay.

George Gammon

Not that it’s investing advice or anything. The other thing that people might find interesting is I’m long a ticker symbol called DXT. Okay. Now what DXT is, is it’s long the Nikkei.

Monetary Metals

Okay.

George Gammon

But it’s got a dollar hedge, ah, or basically a yen hedge. So if the dollar goes up against the yen, you’re most likely going to win on And if the Nikkei goes up, even in nominal terms, you’re most likely going to win on that.

Monetary Metals

I see.

George Gammon

So you see what happens if let’s say you’re a Japanese citizen and you know yen’s going to 200, what the hell are you going to do? You’re most likely going to put it into the market of stocks, right? Something that tries to get some kind of appreciation. Yes. Or at least protects your purchasing power.

Monetary Metals

Right.

George Gammon

So you could have a nominal increase in the Nikkei. And then as an American, your currency is the dollar. So you’ve got that hedge in there so you don’t take the FX risk. It’s actually a little bit—if the dollar does go up against the yen, that actually is a tailwind to the overall ETF, or however it’s structured. Yeah.

The other thing I like about—a good friend of mine is named Hugh Hendry, and he’s a former hedge fund manager. And one of his favorite charts was a long-term breakout from a prior high. But when he’s talking about a long-term break, he’s talking about like decades, not like just last year or something like that. So if you remember, The Nikkei topped out in 1990, but it exceeded—it broke out. It was like a year and a half ago.

Monetary Metals

Okay.

George Gammon

It broke out. So you got to think about that. That’s a 35-year chart where it broke out after 35 years. And for Hugh Hendry, that, that would be one of the most powerful charts he’s ever seen in his life because it’s a powerful signal of a fundamental change, like a fundamental sea change happening in that market. Yeah. That you can tell just by the technicals.

Monetary Metals

I see.

George Gammon

Right, that for all this time, you know, the Nikkei has been dead money, right? And something has triggered it to where it’s not only got back up to that prior high, but it’s exceeded that and it stayed higher. A lot of times you get something like that, it continues to go higher for the next decade or 15 years or something like that in nominal terms, right? So I like it for the technicals, and I like it because the dollar-yen, and I like it as kind of like a local inflation hedge going into the stock market. And that’s probably something that most people It’s not on their radar.

Monetary Metals

Okay. So is it fair to say 6 to 12 month outlook, George Gammon, ultimately dollar bullish, relative dollar strength to foreign currencies, foreign markets? Curious in that thesis, like what’s the one or two things that might cause you to change your mind? Like what would it take for you to take a different stance?

George Gammon

So to answer your question, I would really focus on the US Treasury curve. So as an example, right now the delta between the 2s and 10s is about 40, 45 basis points. That’s very unusual. That’s a flat curve. Now, it’s not inverted again like we were 2 years ago, but that’s a really flat curve. So what you would expect in a healthy economy is the 10-year Treasury to probably be, let’s call it, 100 to 150 basis points higher than the 2-year.

There’s 2 ways it can do that. It can do that for a bull steepener, which would be very actually bearish to the economy. A bull steepener is when the 2-year Treasury would, let’s just say, go down 150 basis points. While the 10-year stays the same, that would mean the economy is not in good shape, right? And that would be most likely dollar bullish.

But then if we see the 10-year Treasury go up, and let’s just say the 2-year stay the same, then it would be the exact opposite. Because what that’s telling me is that growth and inflation expectations are increasing, and the economy is starting to do better and better and better and better and better and better and better.

And if the US economy is doing better and better and better, you kind of use as a proxy for the global economy. And then I would assume that the amount of dollars that are being created are going to, you know, pick up just like we saw in 2000, and we’re kind of off to the races. That would be an absolute best-case scenario.

And if that did happen, if we saw like a bear steepener where the 10-year goes up to like a 150 basis point delta, I would actually go from being probably dollar bullish to dollar bearish. And I would be more bullish on the economy—more bearish now—and I would be more bearish on the dollar, and then I would be more bearish bearish on interest rates, meaning I would go from thinking that interest rates probably have a downward bias to having an upward bias.

Monetary Metals

Okay. Yeah.

George Gammon

So if you put a gun to my head and said, you know, a year, what do you think the 10-year—I think the 10-year is going to be lower than it is. I would say the 2-year as well.

Private credit could be the next subprime

Monetary Metals

Quantify that, like, by when you say lower, like, like 20, 50 basis points?

George Gammon

Oh, I have no idea. Okay. I have no idea. It just, it depends, you know, it It depends on what happens with the labor market. And I mean, the cycle right now seems to be playing out very similar to 2008, where you have the CPI going up, you have oil going up, and that’s kind of the catalyst that brings on an economic contraction that inevitably leads to actually disinflation and the Fed dropping rates to zero.

And will that happen again? I don’t know. If I had to look at one kind of usual suspect right now, I would look at subprime, but this cycle it’s not subprime mortgages. It’s subprime private lending.

Monetary Metals

I was going to ask, like, what’s the one indicator to look for? I was going to say maybe credit spreads.

George Gammon

Yeah, you can look at corporate credit spreads, nonfarm payrolls. Yeah, I would focus on that. I think if you just focus on those two things and the yield curve, you’ll be doing all right.

Monetary Metals

And what are those things currently showing? Are they showing—you know, they’re not necessarily sending out alarm signals now, but you’re in a mode where you’re paying attention to them?

George Gammon

Like, yeah, I mean, corporate credit spreads are kind of up a little bit, but Not that big of a deal.

Monetary Metals

Anything crazy?

George Gammon

Private credit’s really something to look at. I don’t think we’ve seen the last of that. But, you know, you got to remember that we saw the whole thing collapsing at the beginning of 2008. And that really—and still from March to June, interest rates went up by 100 basis points before they came crashing down. So the timing of this stuff is really difficult.

Monetary Metals

The other thing about private credit to me, I’m curious to hear your take on this, like how contained is that?

George Gammon

Oh, it’s not contained.

Monetary Metals

So it falls in that category of like contagion risk, right? Like this is—if you have this asset class breaking down, the collateral damage is going to spill out into other areas versus like a more localized contained crisis. I’m thinking like commercial real estate, right? Like that was blood and guts in the streets but didn’t really have the impact that—

George Gammon

Yeah, but it still is. There’s no way he’s talking about like—can you just do his presentation on that? How he’s buying things at like 50 cents? It is down.

Monetary Metals

I guess what I’m kind of always referencing back back to the GFC, right, where you had like broad-based selling off all asset classes.

George Gammon

Yeah, yeah.

Monetary Metals

But the, the initial kind of catalyst was subprime. Subprime. That’s kind of what I’m getting at. Yeah, I’m just curious to hear your take on that.

George Gammon

Yeah, so a couple different ways to look at this. I think the wrong way to look at this is say, okay, mortgages were whatever, you know, a $30 trillion market, and therefore you can’t compare it to private credit because private credit’s $2 trillion. That’s the wrong way to look at it, because what we have to remember is that although it was a, let’s just say, $20 or $30 trillion market only, I mean, it was like 5% of the mortgages went into delinquency and then default.

Monetary Metals

Really? It was that low?

George Gammon

Yeah. Yeah.

Monetary Metals

Wow.

George Gammon

Okay. Yeah. See, it surprises you, right? Yeah. Like if I asked you, you’d probably say, oh, 20 or 30%. It was actually a very, very small percentage. And most of the mortgage-backed securities actually made money. Right. So how—what happened? It was really just psychological because what you’re doing is you’re taking a monetary system that is dependent on not only the circulation of credit, but that circulation of credit is dependent on collateral. And the main two sources of collateral are mortgage-backed securities and treasuries. Right. So if you have this much collateral and overnight it goes to this much collateral, you got a big, big problem.

Monetary Metals

Right.

George Gammon

Right. Even if—and was it rational to take out all the mortgage-backed securities as far as collateral? It was probably rational, but it ended up only, you know, 5% of them blew up. Right. So you could have left 95% in there. And you still would have been fine, but no one wanted to do that because you didn’t want to touch mortgages with a 10-foot pole because you know how to price it.

Monetary Metals

And meanwhile, everyone’s just, you know, running to the exits.

George Gammon

Yeah. So then what happens is the economy is all about the circulation of money and credit. So if you have a big scare like that, even if it’s just all psychological, it doesn’t matter. The net result is still the same, right? And that if you have a frozen monetary system, the plumbing freezes there’s no circulation of money and credit, and everybody blows up because there’s no liquidity.

And it was just a result of the psychological process that was triggered by, let’s just say, 5% of the mortgages blowing up. So my point there is it doesn’t really matter the size of the $2 trillion, you know, private credit, $20 trillion. It’s if the psychological impact is the same, the result will be the same.

Monetary Metals

And so what do you think? Do you think private credit has the potential to have that same psychological impact?

George Gammon

I think it does. I think it definitely has the potential because you get a feedback loop, right? And people talk about private credit and software, but they didn’t just invest in software. I would talk to Kenny, I’m like, where are all these guys getting the money to build at $350 a square foot when they really shouldn’t have been building at anything over $250 a square foot? It’s like they got all from private credit. It’s all private credit. So it’s not like their balance sheet other than software is pristine.

They’ve got subprime auto on their balance sheet. They got software on their balance sheet. They got multifamily on their balance sheet. It’s having to be sold for 50 cents on the dollar. And we haven’t even seen that surface. The only reason you know that is because I talked to guys in the trenches like Kenny, a big multifamily guy that runs $3 billion in multifamily. And you talk to guys with boots on the ground and they sit there and tell you a much, much different story than you’re hearing in the mainstream mainstream media or those private credit guys that go on CNBC would lead you to believe.

Sure. You know, they’re always like, oh, nothing to see here, nothing to see here. And then like, oh, we’re valuing the assets on our balance sheet at 98 cents on the dollar. And like, according to whom?

Monetary Metals

Right.

George Gammon

Like, well, us, our own models. Well, we just—and they say, well, look, we just took this loan and we just sold it at 98 cents on the dollar. Like, really? Who was the buyer? Like, oh, you know, that’s a subsidiary of ours. Oh, so it was you that bought it from you at $0.98 on the dollar. Now you’re claiming it’s actually worth $0.98 on the dollar. I see how this game is played.

Monetary Metals

Right, right, right.

George Gammon

It’s like a shell game. It’s just like this. And they’re just trying to kick the can down the road. And, you know, sooner or later you get to the end of the line and it’s time to pay the fiddler.

Monetary Metals

That raises the last question. We’ll end with this one. So going back to GFC, everyone’s rushing the exits, flight to safety, flight to liquidity. Gold sells off.

George Gammon

Yeah, yeah.

Monetary Metals

They sell gold. It’s another asset, high-quality asset, highly liquid. It’s a way to get dollars. Just kind of gaming this out a little bit, if private credit collapsing takes a similar turn there, does gold behave the same way?

George Gammon

Probably.

Monetary Metals

Is it as steep or is it less? The question behind the question is, is the gold market today—is the flight to safety to gold as another safe haven asset, has that changed materially in the last No, no, no.

George Gammon

Gold’s still doing its job. But the thing is, to your point, its job is to provide liquidity when there’s no other liquidity. So that’s why gold goes down during the GFC. That’s why gold goes down during a 2-week period during COVID because you got to sell anything on your balance sheet and no one’s willing to buy anything except for the gold. Sure. So the gold is doing what it’s, it’s supposed to do. It’s the flight to safety. It’s the no counterparty risk. It’s in an emergency.

You got to have something and it’s, it’s bailing you out, right? But the net result of that is the price goes down temporarily. And notice I said temporarily, right? Because then what happens is eventually you’re going to come back. And usually the way countries or, you know, governments come back is just through a Keynesian approach of just—yeah, this massive fiscal and all this nonsense.

And then, you know, you look back at gold and that’s usually when it rips. I mean, I can’t remember when gold tanked in 2008. I think it was probably after Bear Stearns or something like that in the summer. It goes down, but then you look at it from, you know, December of 2008 to like the middle of 2011, it just ripped. I mean, it just went absolutely parabolic.

Monetary Metals

Within 6 months, it was already back in an uptrend, pretty sure.

George Gammon

Like, oh yeah, and then it, then it actually turned into a bubble, right? Right.

Monetary Metals

And it ran really hot for a while, right?

George Gammon

Yeah, yeah. But I would expect the exact same thing to happen, you know, if you have a blowup in private credit that takes gold down with it, like a similar V kind of Yeah. So we’re at 45 today. You know, figure it goes down to, you know, let’s call it 38. But then a year later, you’re at 7,500.

Monetary Metals

Okay. Well, that’s a good place as any to end.

George Gammon

Yeah.

Monetary Metals

So I really appreciate you taking the time with us, George.

George Gammon

Thanks.

Monetary Metals

Thank you so much.

Follow Monetary Metals on X: @Monetary_Metals

Follow George Gammon on X: @GeorgeGammon