Continues here

BofA: Taking a pause – but we think gold will rise again

The Fed can slow gold down. It cannot erase why central banks are buying it.

- What BofA Says

- The Fed Has Become the Immediate Problem

- ETFs Are the Tell

- Central Banks Are Still the Anchor

- The Dollar Problem Has Not Gone Away

- GoldFix Read

What BofA Says

Authored by GoldFix

Gold’s bull market is taking a pause, but BofA does not believe the larger story is over.

In its June 19 Global Metals Weekly, BofA Global Research, led by Michael Widmer, argues that gold faces a tougher near-term setup because the market has moved away from the clean “inflationary cuts” narrative that powered the original rally. The old setup was simple: inflation remained above target, the Fed was easing, real rates were moving lower, and the dollar was under pressure. That was the best possible macro weather for gold.

That weather has changed.

BofA says expectations for tighter monetary policy, renewed dollar strength, weaker ETF flows, and the possibility of future Fed balance sheet reduction have created a near-term overhang. The bank now says its prior $6,000 per ounce target looks unlikely “for now,” even though it still sees the longer-term case as intact. The reason is not technical. It is structural. The United States still has large deficits, no meaningful fiscal consolidation, rising funding needs, and declining foreign participation in Treasury markets. Those were the original ingredients behind BofA’s bullish gold call when gold was closer to $1,900 per ounce. They remain in place today.

“Taking a pause, but we think gold will rise again.”

That is the report’s core message.

The Fed Has Become the Immediate Problem

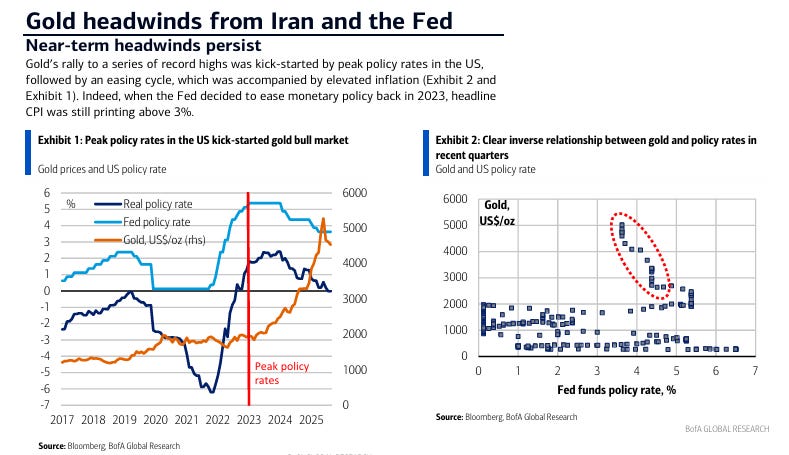

BofA’s near-term gold concern starts with the Fed.

Gold’s surge began after policy rates peaked in 2023. The key point is that the Fed began easing while inflation was still above target. That combination, according to BofA, laid the foundation for the bull market. Gold likes easing. Gold likes negative real rate pressure. Gold likes policy credibility questions. Gold especially likes all three at once.

But the June FOMC meeting changed the market’s interpretation. BofA notes that nine policymakers projected rate hikes this year, inflation forecasts were marked higher, and Chairman Warsh leaned hawkish by emphasizing price stability. The report says the absence of dovish language mattered. The Fed is no longer signaling that it will “look through” inflation caused by tariffs, supply chains, energy shocks, or geopolitics.

That is important because gold does not just trade on inflation. It trades on the policy response to inflation.

Inflation with cuts is gold-positive. Inflation with hikes is less powerful.

BofA quantifies that shift clearly. A move from inflationary easing to tightening reduces potential gold upside by roughly half. Since 2001, gold’s year-over-year gain during inflationary easing periods has averaged 21.8%. During inflationary tightening periods, the average gain falls to 10.8%. That is still positive, but it is not the same impulse.

Inflation is bullish for gold when the Fed is easing. It is less powerful when the Fed is hiking.

In plain English: gold can still rise with a hawkish Fed, but it has to work harder.

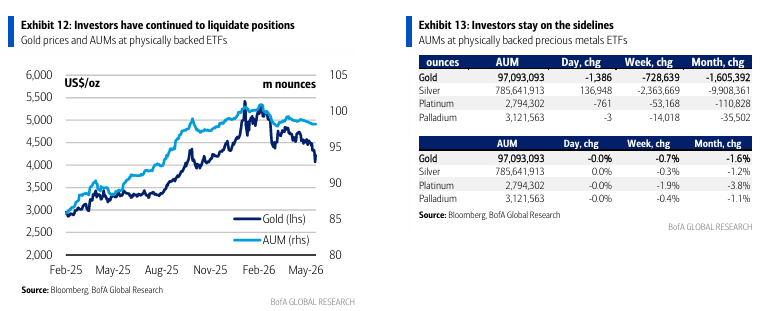

ETFs Are the Tell

The report treats gold ETFs as the cleanest proxy for investor appetite.

That is not because ETFs control the whole gold market. They do not. But they are highly visible, highly liquid, and they give a real-time signal of Western institutional interest. On that measure, BofA says investors have continued to liquidate positions. Physically backed gold ETF assets fell by 1.6% over the prior month, with gold ETF holdings at roughly 97.1 million ounces in the table shown in the report.

ETF flows are the tell. Western investors have not yet returned to the trade.

That matters because BofA’s prior bull case had two pillars: macro stress and investor allocation. The macro stress remains. The allocation impulse has cooled.

Free Posts To Your Mailbox

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

Loading...