Uranium: Cameco's Safety Buffer Used Up

Cameco has temporarily halted mining at Cigar Lake following an acid plant failure at Orano's McClean Lake mill, where the ore is processed. Cameco expects the mill back online within two weeks and sees no impact on 2026 guidance for now, though this remains at risk if repairs take longer than anticipated or alternative acid supply cannot be secured in time. We suspect Cameco is pursuing alternative acid supply in parallel with the repair in order to restart milling sooner and limit the risk to 2026 production guidance.

Following our report on the bridge collapse impact at McArthur River in May, we reiterate that Cameco's 2026 guidance is hanging by a thread, both on production and spot market purchases. McArthur River resumed operations faster than we had anticipated, which limited the impact there. Now we have this.

Implications for Guidance and Spot Purchases

Assuming this fully resolves in two weeks as guided, the impact would be c-0.7Mlbs. We think this together with the McArthur bridge disruption mean production for the group in 2026 could be towards the lower end of guidance range at c31.9Mlbs (100%).

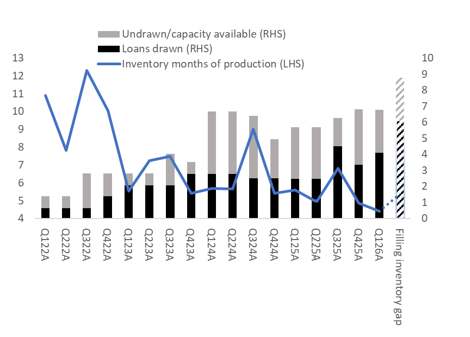

As discussed in our Q1 post view, the issue is that Cameco’s inventory coverage is already very low at 4.4 months of production as at Q1. Taking this level back to what Cameco used to see as a reasonable inventory coverage of around six months of production would suggest a current inventory deficit of c2.7Mlbs.

Assuming Cameco could borrow 2Mlbs of incremental uranium now vs Q1, and that it must pay off the 0.75Mlbs uranium loan it took in Q1 maturing this year, then this new outage, together with that of McArthur River would require 3.0Mlbs of spot market purchases this year exactly at guidance’s 3.0Mlbs.

We would be surprised to see Cameco able to borrow more than 2Mlbs incremental vs Q1. We would argue that a generally tightening credit market could finally make product loans less accessible and flexible than they have been previously. A more limited access to product loans would mean filling the supply gap through more spot market buying.

Our base case estimate of Cameco 2026E spot market purchases (assuming 14-day Cigar Lake disruption + 2 Mlbs incremental borrowing), Mlbs

Source: Asymmetric Research estimates, Cameco

Cameco inventory coverage, product loans and facilities, and implications of filling inventory coverage shortfall (months / Mlbs)

Source: Asymmetric Research, Cameco

This is all to say that while Cameco has time and time again demonstrated operational excellence, delivering positive surprises, the margin of safety on its 2026 guidance metrics is now, in our view, depleted.

Any additional delay beyond this would necessitate more spot market buying, in our opinion. To illustrate, a 30-day delay beyond the guided two weeks would imply 1.5Mlbs of additional spot buying from Cameco – which are unaccounted for in its 3Mlbs spot purchase target for the year.

We are constructive on uranium, and have written extensively on the topic over the past few months, where we looked in detail at how: 1) Middle East conflict will prove highly beneficial to uranium, 2) Kazakh strategic reserve could keep Kazakh production lower than expected for the years to come and 3) utilities could begin restocking in the next 2-3 years which is pure optionality but a game changer to the bull case if it were to happen.