Another Cloud Competitor

Welcome to MktContext! I am a professional money manager, trader, and investor who has been timing and beating the market for over a decade. We specialize in predicting market direction by studying the economy and market signals. Join 13,000 subscribers at MktContext.com for our weekly deep dives and analysis!

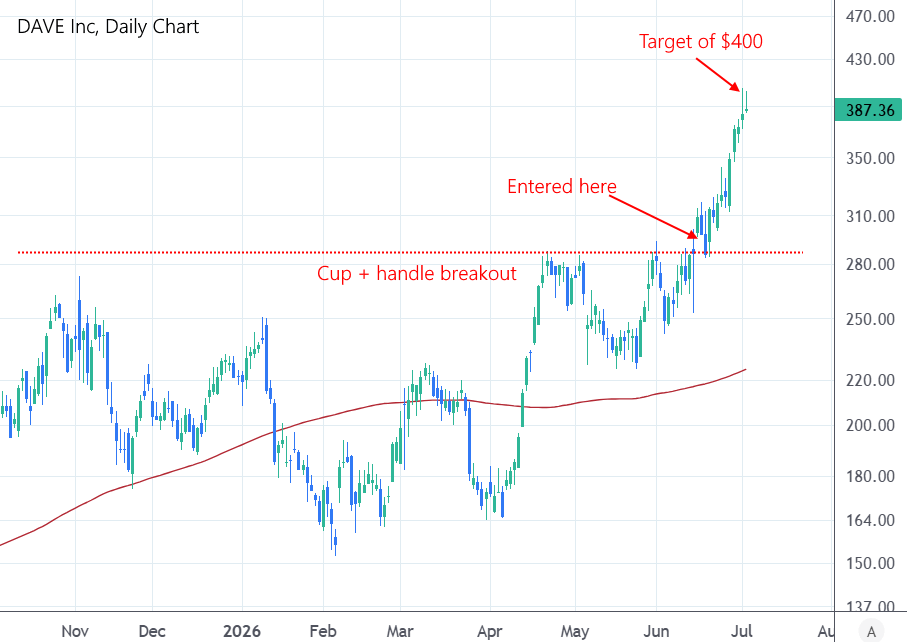

DAVE, the fintech company we picked in our June 14 letter, has reached its price target of $400. From our entry price of $293, this is a 37% move in two weeks. We had taken partial profits along the way, and are now selling most of the stake, leaving a tiny portion for further upside (“runners”).

As we’ve highlighted in the past few weeks, we are in the midst of a bull market rally and rotation into non-tech parts of the market. This is why cyclical stocks like DAVE are breaking out to new highs. We continue to find excellent trade opportunities to capitalize on this trend.

Another Cloud Competitor?

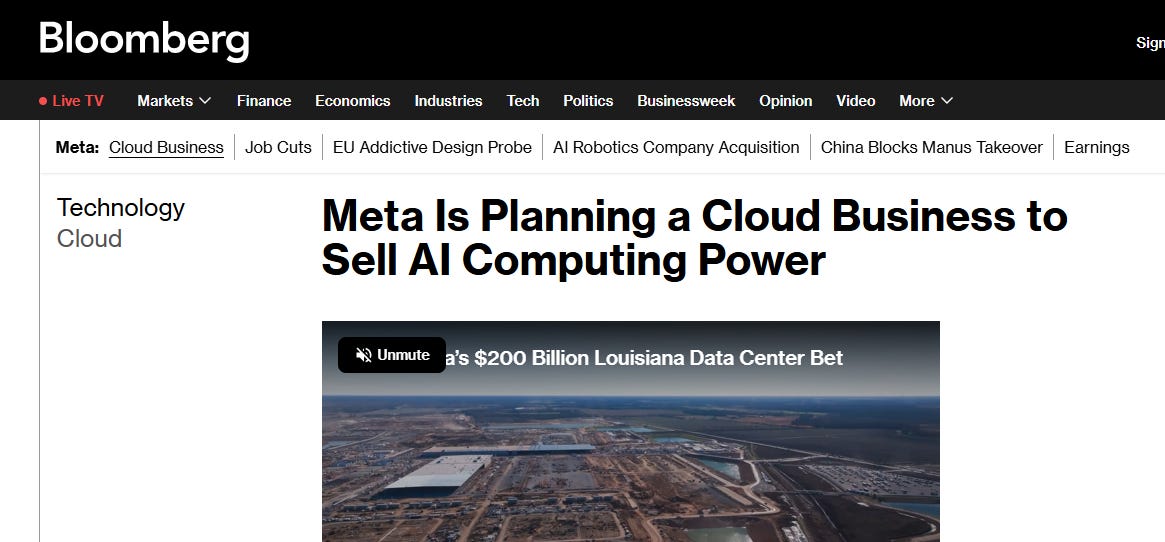

Last Wednesday, Bloomberg ran an article that suggested Meta (parent company of Facebook and Instagram) is starting a cloud business to rent out its excess computing capacity. Investors read this announcement as a signal that they have too many data centers, so CEO Mark Zuckerberg is pausing capital spending. As we’ve written before, Meta has a spending addiction when it comes to AI infrastructure. That’s why META stock shot up 10% on the day the article was published.

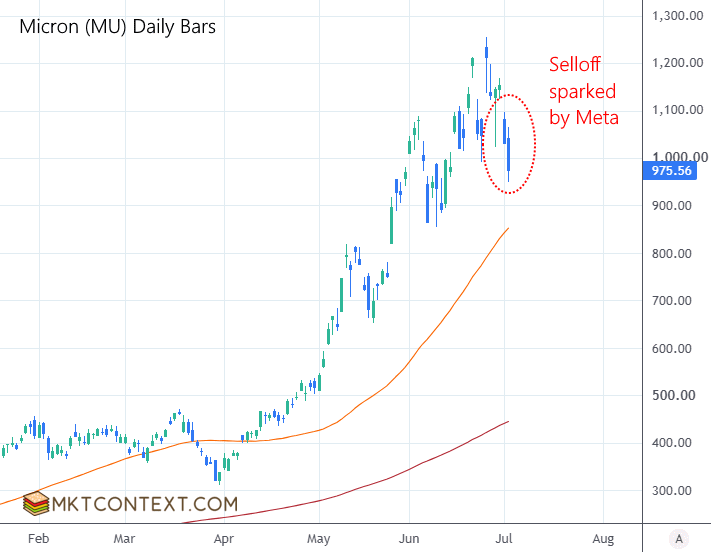

Less spending is good for all Mag 7 since the market extrapolated the cuts to other cloud providers (as we expected they would). On the flip side, less spending means less revenue for data center providers and chip makers, in particular the memory chip makers (chart below). This sparked the selloff in tech stocks that started on Weds and continued into Thurs:

Let us first point out that the reaction may have been exaggerated. Meta is opportunistically taking advantage of current high compute prices. This does not mean they stop building data centers, as their long-term strategy is centered around growth in AI. It also does not mean they stop building their internal AI model, “Muse”.

We’ve been calling for Mag 7 to pull back on AI spending, but this is not it. Unfortunately, the spending addiction continues. If anything, it proves that demand for underlying compute is still red hot.

So what should we take away from this? Recall Encroachment Theory, which we started writing about in March 2025. Mag 7 used to have separate monopolies, but now they are all converging on the same turf. Competition is heating up as AI increasingly proves to be undifferentiated.

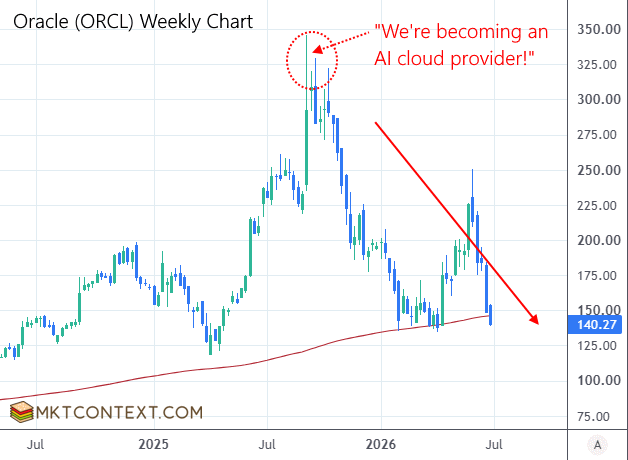

Worse yet, brand new competitors are entering the fray. Oracle is infamously transitioning into an AI cloud provider (look how their stock price is performing). Neoclouds like CoreWeave and Nebius came to market on the premise that demand for AI data centers would outstrip supply for years. SpaceX is building data centers in space. And now, Meta wants to compete for the same customers.

Every seller of excess capacity makes it harder for the next data center/cloud company to justify a premium price. What was supposedly scarce is being answered with new supply. That’s how supply and demand work. The dot-com bubble followed a similar arc: first excess demand for a new technology, met by new supply, and then oversupply.

Get the rest of this article, including our portfolios and trades, at MktContext.com!

Join 13,000+ investors who are timing the market!