EU Natural Gas: Running Out of Time

TTF has rebounded by 20% over the past two weeks. Importantly, around half of that move began before the recent resumption of hostilities around the Strait of Hormuz, including the attack on an LNG carrier. The market is finally beginning to focus on the storage issue we have been flagging since our March deep dive, yet politicians remain in denial. Injections have now been noticeably weak for three weeks running, and withdrawals are higher on continuous heatwaves. We remain long TTF futures.

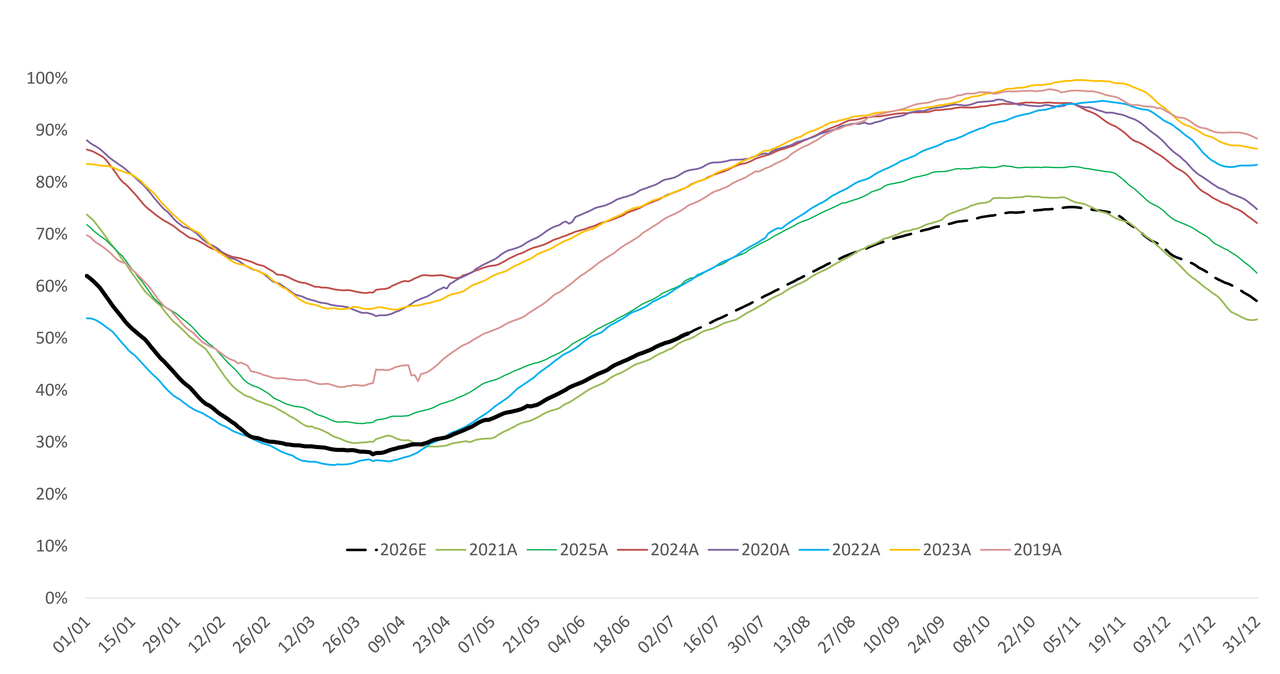

Forecasters are now converging on our numbers. The IEA has followed WoodMac in revising its projections towards what we have been saying for months: peak EU storage this winter will likely mark a 15-year low of around 75% in November, at the EU's flexed lower target. European to Asian price spreads are also not incentivising refill, further weighing on any resolve. Our revised storage forecasts as things stand are shown below.

European Natural Gas Storage Levels and Our 2026E Forecasts, As Things Stand (% full)

Source: GIE AGSI. 2026E = Asymmetric Research estimates

Downside Risks to the 75% Peak

The 75% forecast implicitly assumes that the traffic through the Strait of Hormuz resumes to June levels as early as next week, and that Qatar does not extend its force majeure beyond the start of September. Given the renewal of Iranian attacks on US bases in Qatar, the risk on both counts has edged up. The renewed cessation of LNG shipments now only adds to the cumulative shortfall.

Even the Regulator Is Now on the Record

ACER, drawing on ENTSOG's Summer Supply Outlook 2026, has warned that the EU will need significantly higher LNG imports this summer to refill storage ahead of winter. Its guidance to governments, in one line: ACER is telling Member States to closely monitor their storage-filling trajectories in the months ahead and to actively manage the risks in compliance with the Gas Storage Regulation. That is about as close as a European regulator gets to sounding the alarm.

None of this is new to our readers. We have written extensively about this setup in our previous notes. What has changed is that the IEA, WoodMac and now ACER are aligning with our view and numbers. Complacency tends to disappear rapidly once the data becomes undeniable, as it did in 2021/22, and the injection data is becoming harder to explain away with each passing week.

Remember What Comes Next: Russian Gas Fully Phases Out in 2027

As we discussed in detail in our March report, under the EU phase-out regulation long-term Russian LNG contracts are prohibited from January 2027, and long-term pipeline contracts, the majority of remaining volumes, are phased out by September to November 2027. Europe therefore enters next year needing to replace depleted storage, into what we already view as a tight 2027 balance. That is the structural backdrop against which this summer's injection shortfall should be judged.

Demand Destruction Would Be Less Pronounced This Time

A word on what happens if prices do spike. In the last crisis, the release valve was demand destruction: by the end of 2025, EU gas demand had fallen by approximately 60Bcm compared to 2021 levels, a 16% reduction. With European gas consumption having already reset at these lower levels, any price spike from here will likely have a less pronounced impact on consumption, and prices could remain elevated for longer periods. The buffer that eventually broke the 2022 price spiral is simply smaller this time.

European Gas Demand and Demand Destruction Since 2021

Source: Asymmetric Research, ENTSO-G, national TSOs and market operators

Update (Bloomberg, today): Qatar has reportedly paused its plans to rapidly ramp up LNG production following that attack on one of its tankers, indeed adding further downside risk to our already bearish storage forecast.

Something Has to Give on the TTF Price, and Soon

[...]

This article is based on research originally published on Asymmetric Research. Continue reading, including our full TTF price analysis, our positioning on energy and equities, at: asymmetricresearch.substack.com