The Bounce Trap

The Bounce Trap

Friday's selloff exposed a market built on momentum, leverage, and a belief that the AI trade only goes one way.

History suggests the bounce may not be as safe as it looks.

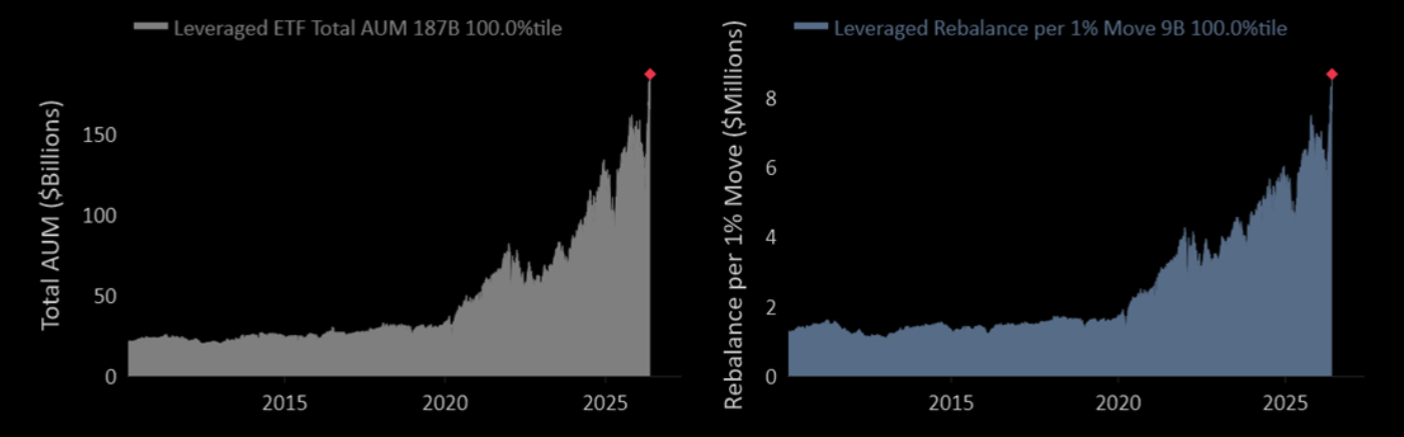

Forced sellers

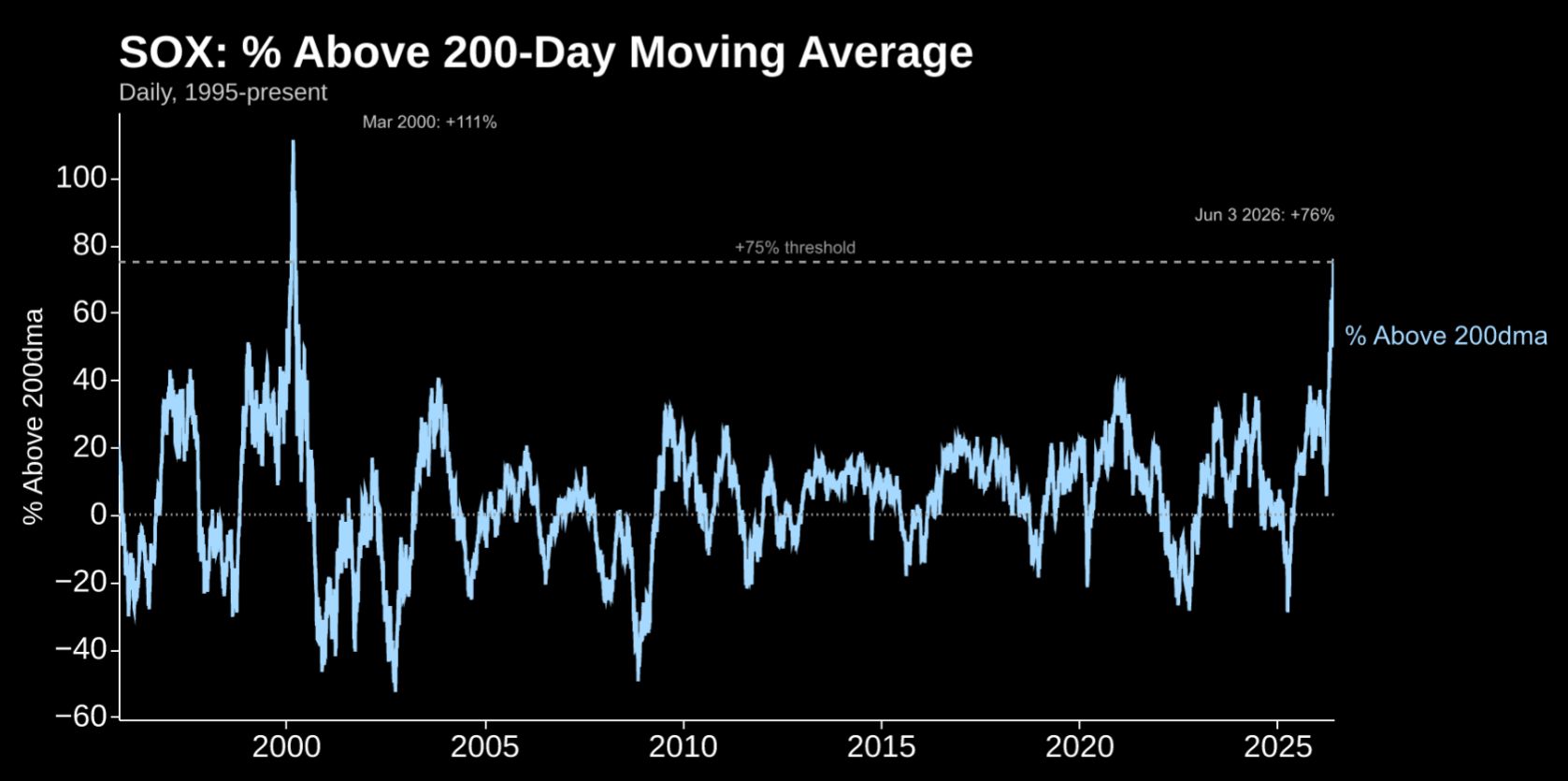

According to Goldman, SOX entered Friday at its most extended level since the dot-com era, trading 76% above its 200-day moving average. One brutal session later, roughly a third of that stretch had already been erased, with the gap compressing by about 22 percentage points.

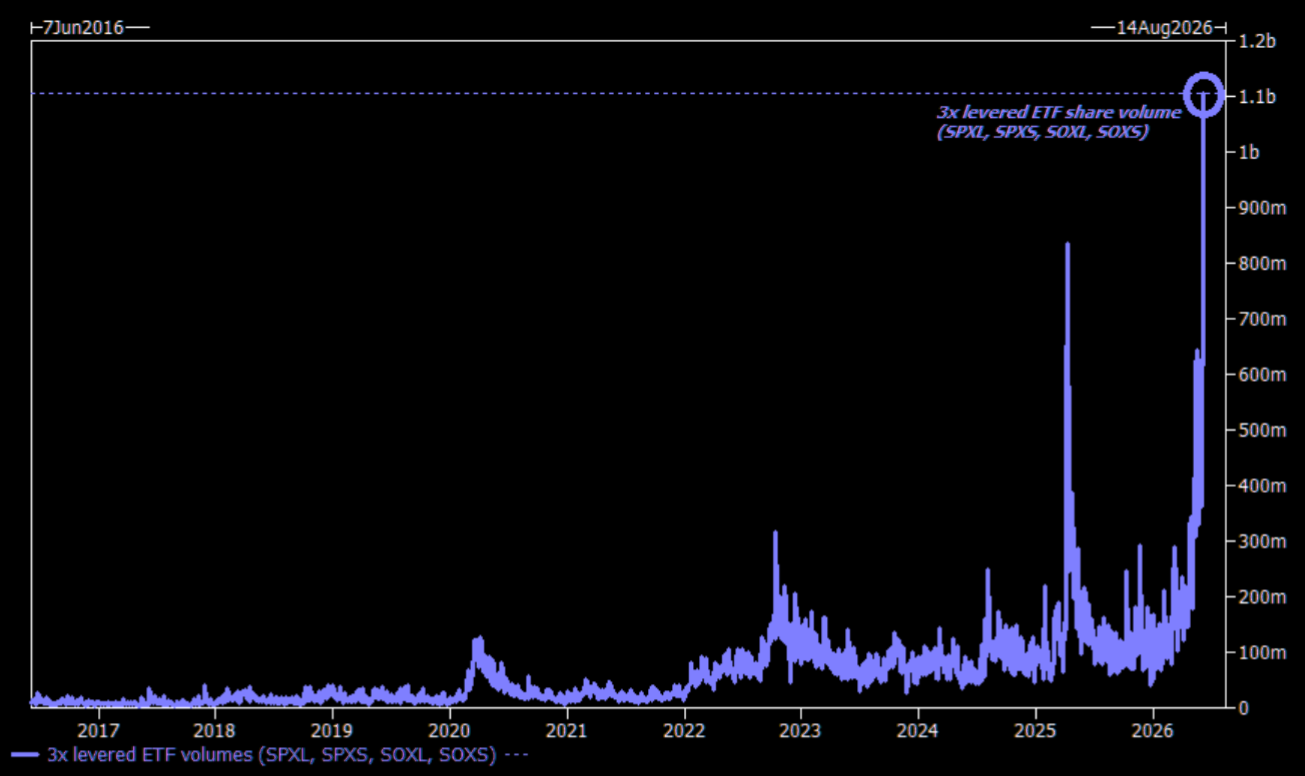

On a related note: Nomura estimates Friday's leveraged ETF rebalance forced roughly $52 billion of selling, led by $23 billion in Semis, $18 billion in Tech, and nearly $5 billion in the Mag 7.

The key point is that these flows are mechanical. In a stressed market, they can quickly become an accelerant rather than a passenger.

Source: GS

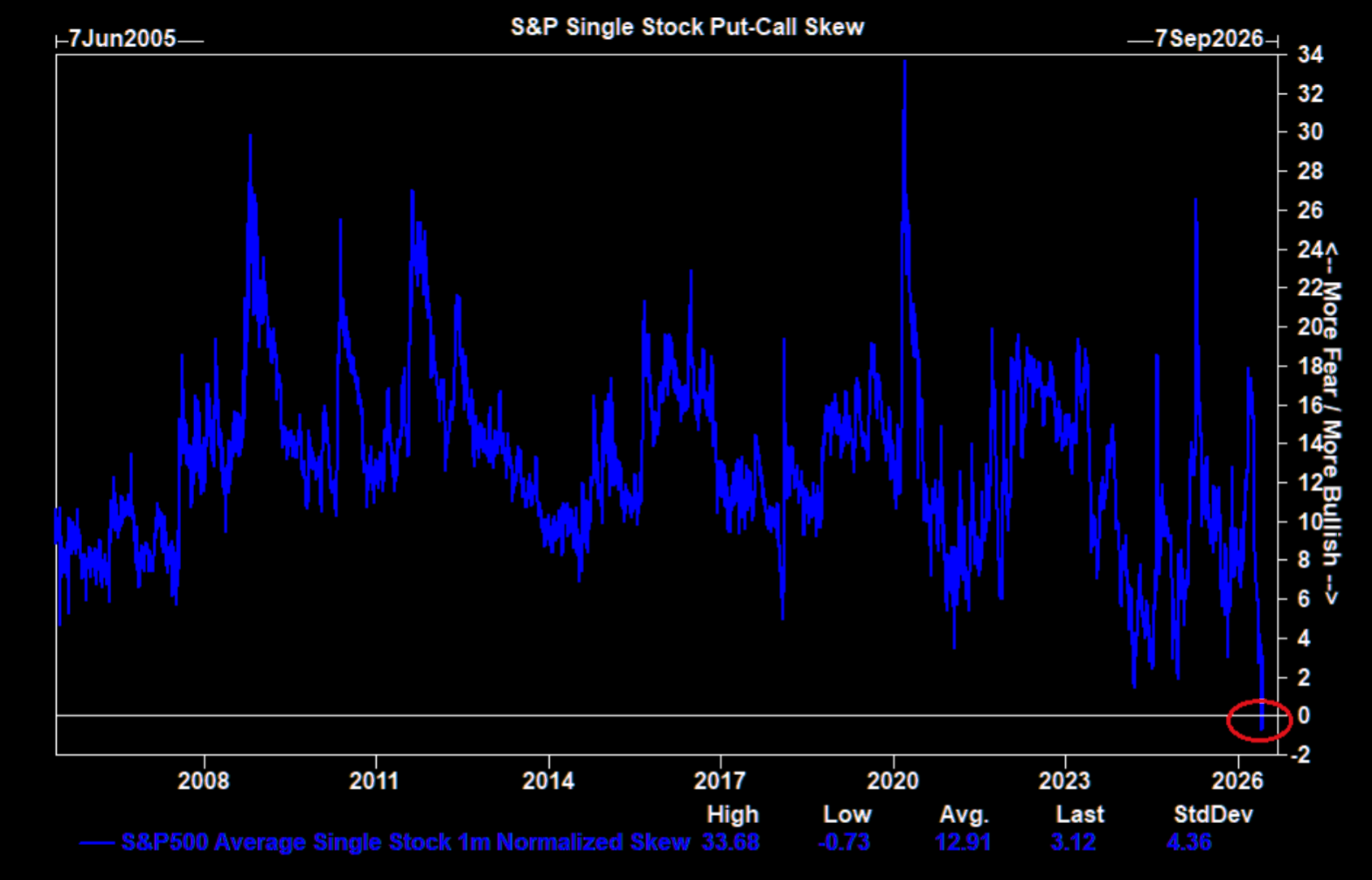

Groupthink

Going into the Friday mess, investors were in "inverse" risk mode, paying up for calls over puts. This is not normal, and the wake up call was expensive.

Source: GS

Synthetic short gamma

Leveraged ETF trading needs a new vocabulary. These products create massive synthetic short gamma exposure that can turbocharge moves in either direction.

On Friday, the mechanism worked in reverse. Falling markets forced rebalancing flows that added to selling pressure, helping turn a sharp decline into an outright volatility event. Latest volatility note here.

Source: GS

Source: Nomura

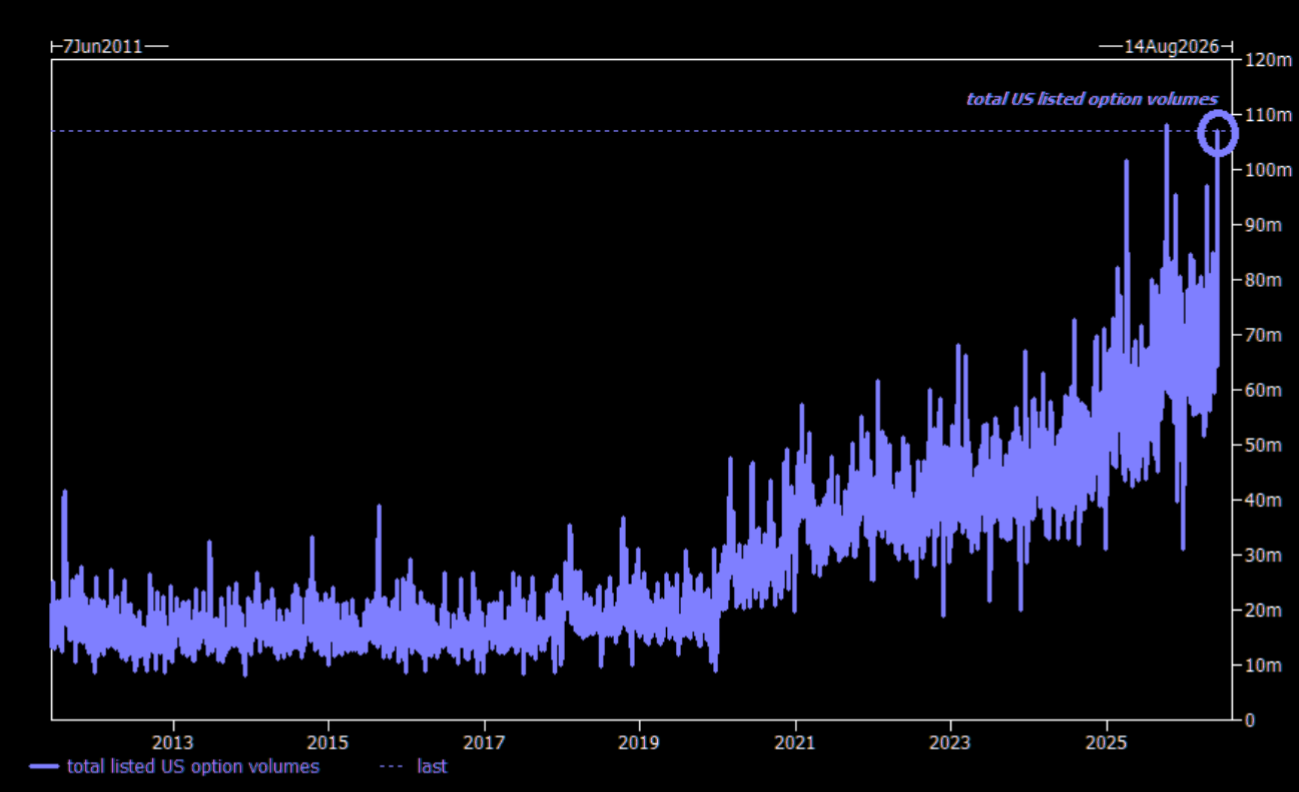

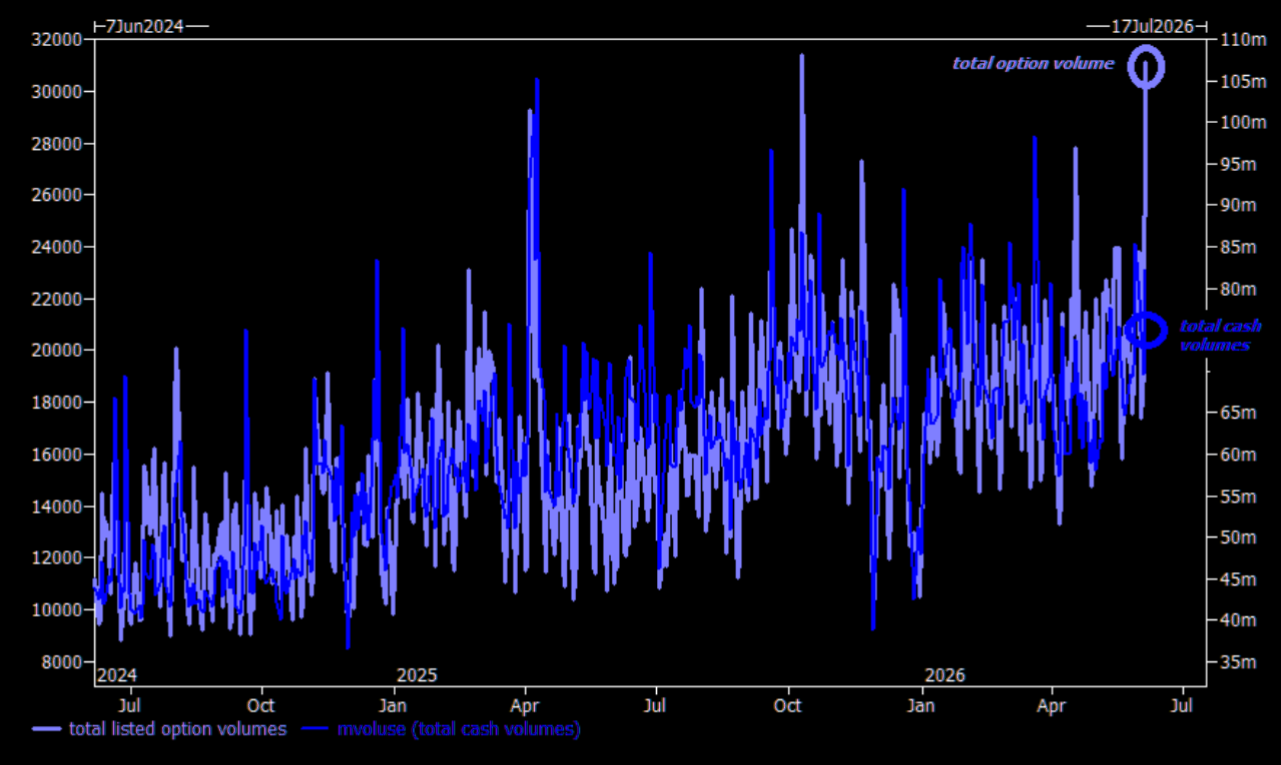

Options mania

Options volumes keep exploding higher. More than ever, this is a market driven by options and the Greeks.

Price action is increasingly being shaped by gamma and other options-related flows, creating feedback loops that can rapidly amplify moves in both directions.

Source: GS

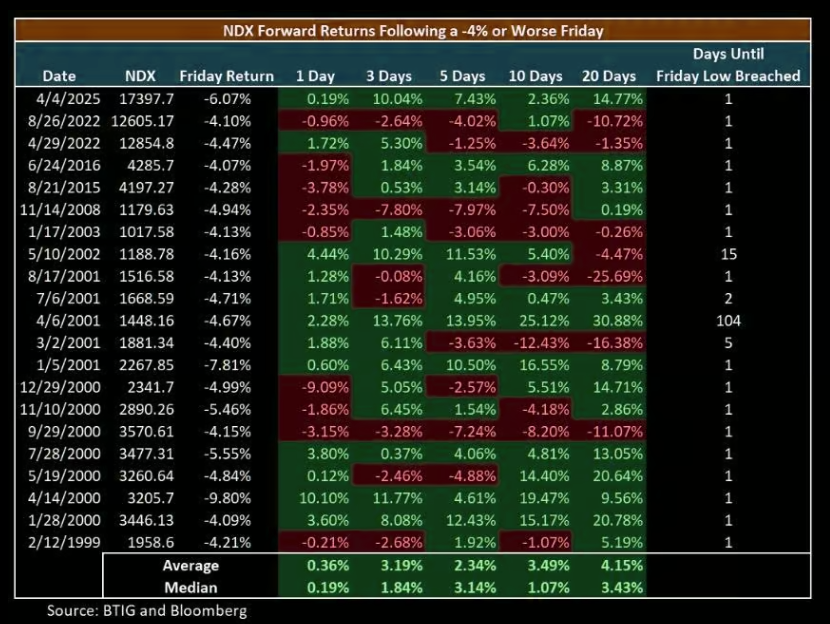

Don't trust the bounce

"....when NDX loses -4% or more on a Friday there is a 90% chance that Friday low is breached in the next five trading days, and we don't think this time is different." (BTIG)

More here.

Source: BTIG

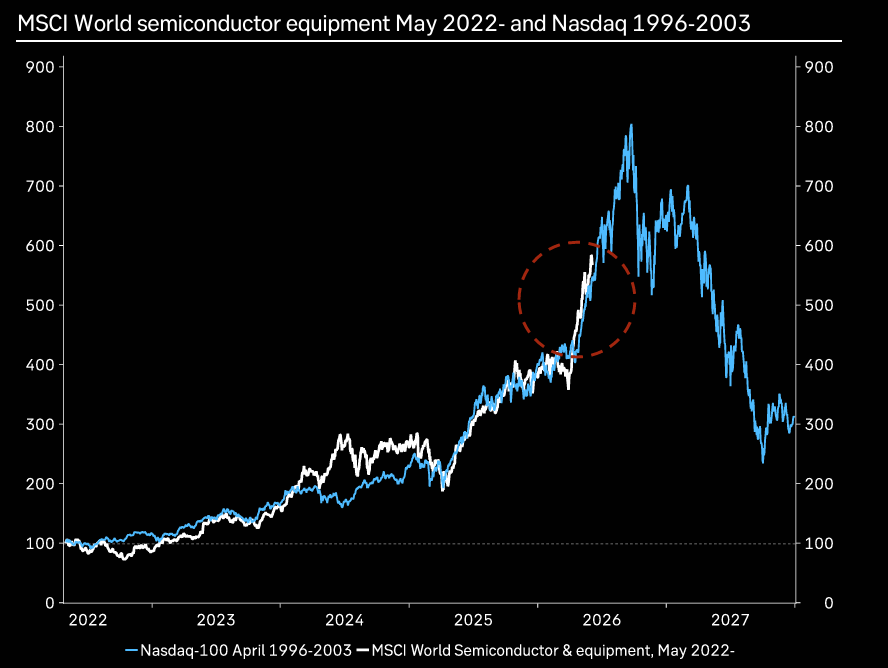

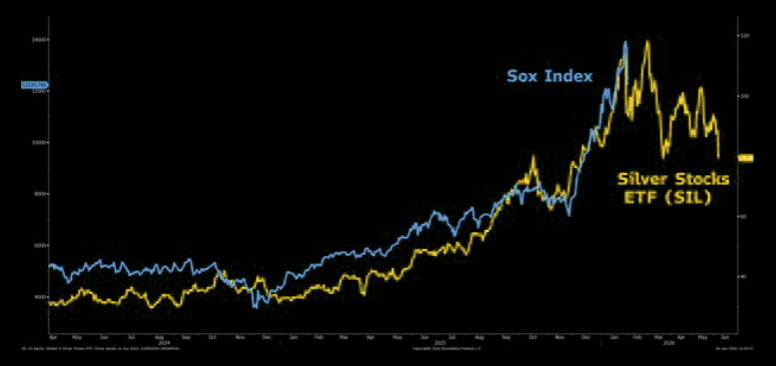

The psychology of manias

There is little fundamental connection between semis and silver. The connection is psychology.

Silver was the hottest trade around until it wasn't. Wilson's comparison is not a call on semiconductors. It is a reminder that markets repeatedly fall in love with a single narrative, a single trade, and a single source of easy gains.

The names change. The stories change. The psychology does not. Full note here.

Source: MS/BBG

The divergence

Oil has been the dominant driver of rates ever since the Iran war broke out. The latest spike in yields is notable because crude has not really confirmed the move.

If rates continue rising without help from oil, this could start becoming a much more serious story.

Source: LSEG Workspace

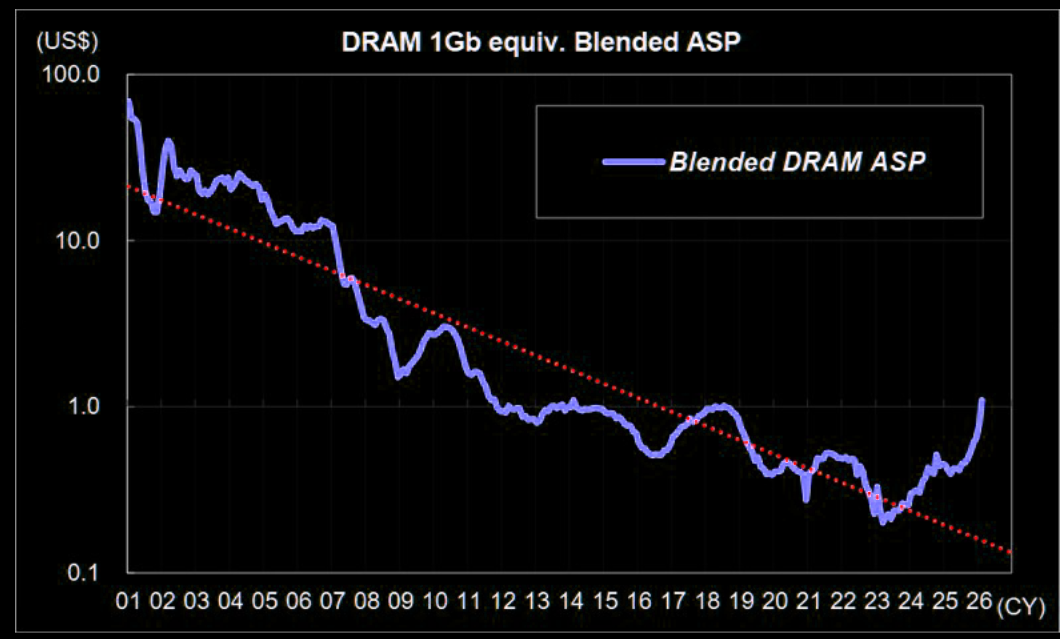

Chipflation

Memory prices have risen more than six-fold over the past year, while the memory market is projected to grow by roughly $600 billion in a single year. The key point is that AI demand remains highly inelastic, creating a hidden inflation channel that traditional inflation measures barely capture. More here.

Source: MS

The bull case

The irony is that some of the most powerful secular bull markets often experience their sharpest corrections along the way. If history is any guide, the semiconductor supercycle may still have another 30% upside left.

The question is whether investors can stomach the path. More here.