Dollar Breakout, Euro Breakdown

Comeback kid

The dollar is dead, long live the dollar. Consensus remains bearish on the USD, yet the DXY is breaking above the key 100 level as we write. We outlined our bullish dollar logic a few weeks (here) ago when the negative trend line was taken out. A close here would break the range in place since May, and the vacuum above that range could get violent.

Source: LSEG Workspace

Huge

100 is huge in the DXY. Note we are now well above the 200 day MA.

Source: LSEG Workspace

The long term trend

Many decided to turn bearish on the dollar right at the massive trend support line.

Source: LSEG Workspace

Euro puking

The euro remains the constant sucker. It has broken decisively below the range and is now trading well below the 200-day moving average. No bueno.

Source: LSEG Workspace

The economy

The Citi EU-US Economic Surprise Index still trades with a wide gap versus the euro, suggesting there may be further room for the soggy euro to move lower.

Source: LSEG Workspace

Topping out

The "dome" euro logic continues playing out well. This still looks similar to what we saw back in 2021.

Source: LSEG Workspace

The oil connection

The last time oil traded around these levels the euro was near 1.02. We are not calling for a crash, but zooming out shows the euro–oil relationship is rather strong. A closure of the Strait of Hormuz would create a structural divergence favoring the USD while exposing the Eurozone to stagflation risks. Higher energy costs would increase pressure on the ECB and could force a hawkish pivot sooner than expected.

Source: LSEG Workspace

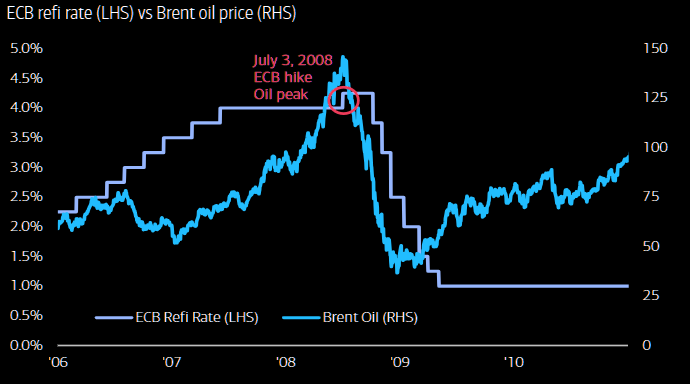

THE mistake

Hartnett Friday poetry: From August 2007 to July 2008, oil surged from roughly $70 to $140 per barrel as subprime tremors spread (BNP, Northern Rock, Bear Stearns). Oil peaked on July 3, 2008, the same day the ECB hiked rates by 25bps, a move widely seen as one of the biggest policy mistakes in modern central banking. Just 74 days later Lehman collapsed and the GFC unfolded, with crude plunging to around $40 as credit stress trumped the oil shock and the ECB was forced to cut rates by 325bps. Today, the probability of an ECB rate hike by June 2026 is around 75%, while Wall Street is increasingly drawing parallels to the 2007–2008 setup.

Source: BofA