Narrow rally as liquidity peaks

NASDAQ de-coupling?

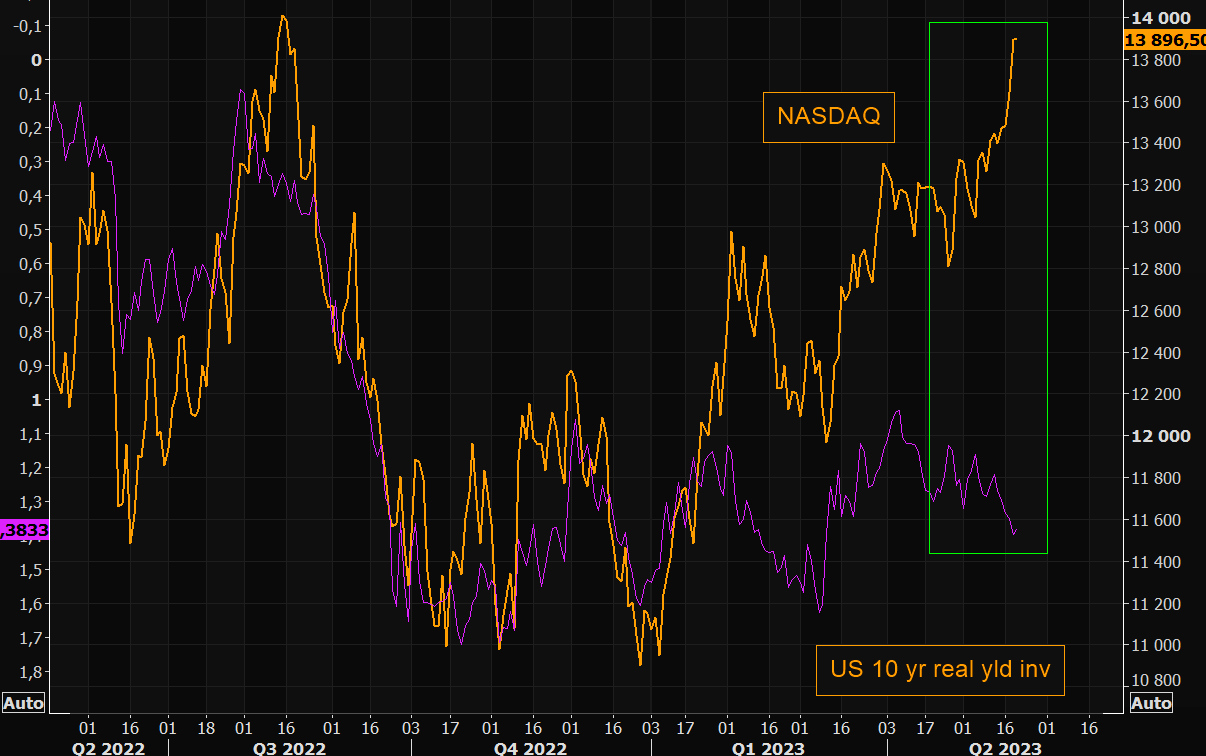

NASDAQ vs the US 10 year real yield (inverted) gap is getting very wide here. Watch this closely as momentum chasing PMs tend to get carried away...

NASDAQ vs the US 10 year real yield (inverted) gap is getting very wide here. Watch this closely as momentum chasing PMs tend to get carried away...

{kind=link}