Waiting for the next direction

Top heavy or mother of all catch-up rallies around the corner?

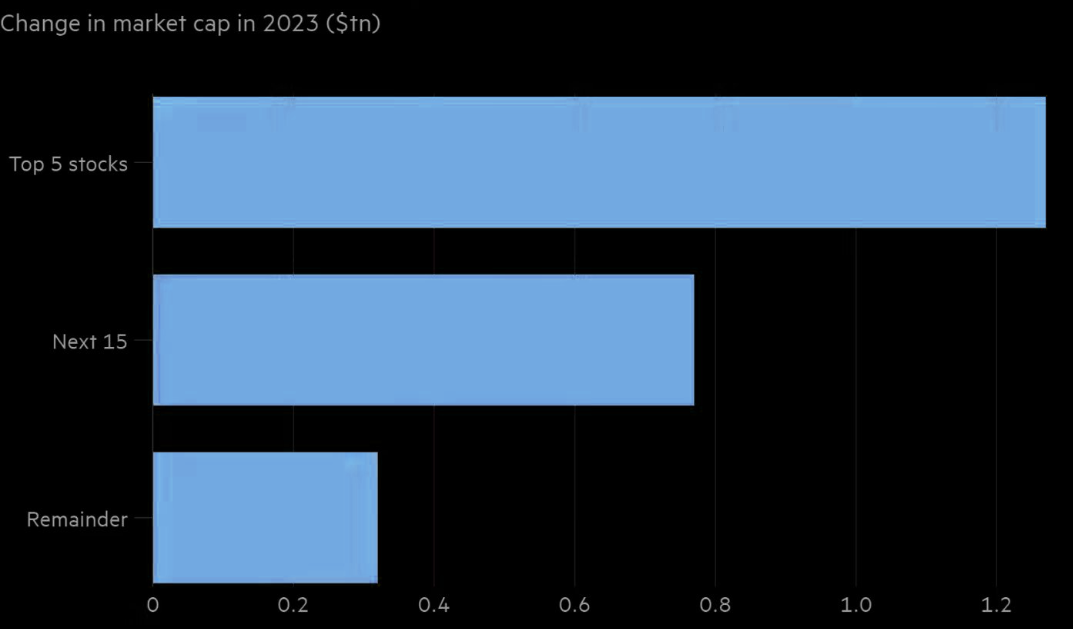

Twenty S&P 500 stocks account for 90% of Wall Street’s gains this year. The rest will now follow...?

Twenty S&P 500 stocks account for 90% of Wall Street’s gains this year. The rest will now follow...?

{kind=link}